In 2006 Microsoft (NASDAQ: MSFT) spent $21.9 billion on the execution of its "red ocean" strategy. What did shareholders get for their money?

This is the second in a series on "Microsoft's $154 Billion Question" and the 7th in a series on corporate brands in enterprise marketing. In this post I map enterprise marketing expenses onto the sources of intangible market value and introduce a simple measure of how shareholders know if they're are getting their money's worth on "red ocean" spending.

BRAND NAMES IN ENTERPRISE MARKETING

Corporate brand names play a much more significant role in enterprise marketing than they do in micromarketing. In fact, much of my book "Competing for Customers and Capital" is dedicated to highlighting the larger role of corporate brands and providing directions on how to deal with it. As with the other posts in this series the analysis is based on real-world, real-time examples using published financial data.

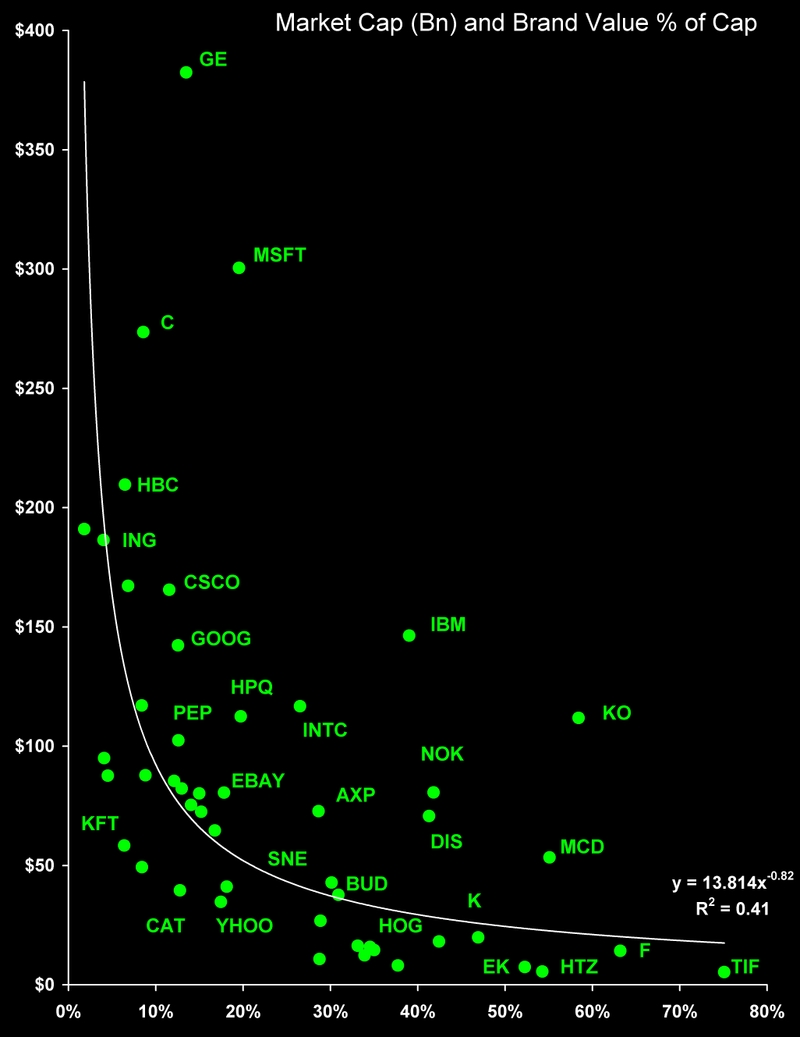

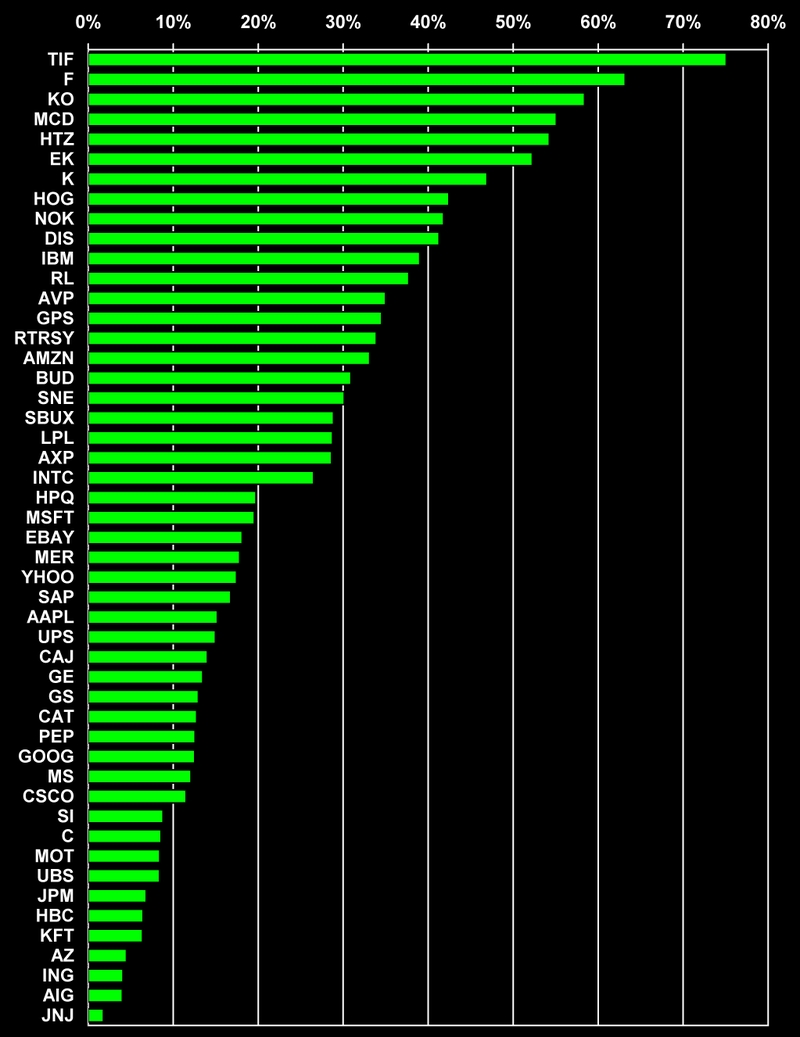

The 1st post in the series was "Sears Brand Bonds," which took a look at how Edward Lampert captured the difference between the book value and the market value of the Sears brand name by issuing brand bonds. The 2nd post applied these ideas to "Coca-Cola's Brand Bonds" to illustrate how the company might create new market value for its 200 lesser known brand names and, at the same time, resolve the ongoing battle with its bottlers. The 3rd post took a marketing oriented look at how to create value by co-branding a company's trademark and ticker symbol in Put a Little LUV in Your Logo!. The 4th one on "Brand Value vs. Book Value" was a broad-brush view of the difference between Interbrand values and book values of 49 of the most valuable brands on the planet. My 5th post in the series took this broad-brush analysis a step further by examining the "Interbrand Value vs. Market Cap" of the same 49 most valuable brand names. The 6th post Accounting for The Unaccountable gave a panoramic view of how all three measures of the value of a company's assets can miss a huge chunk of its market value.

THE DOMAINS OF EXECUTIVE ACTION

Like every other company, Microsoft's revenue dollars may be divided into three parts. I call these Red, White and Blue dollars because they represent three distinct Domains of Executive Action:

• Enterprise Marketing (Red $)

• Corporate Finance (White $)

• Operations Management (Blue $).

The red (enterprise marketing) dollars include all the expenses that drive sales revenue. Some of these expenses enhance revenues by retaining large numbers of existing customers while attracting new ones to the corporate brand. Others diminish revenues by chasing large numbers of existing and new customers away . It's critical to distinguish between the two outcomes. Think of the "Red Ocean Strategy" when you think enterprise marketing expenses.

The white (Corporate Finance) dollars are the earnings left over at the end of each sales cycle. This residual provides corporate financial officers with the discretionary dollars necessary to enhance enterprise value.

The blue (Operations Management) dollars are what it costs to create the product or service before it can be sold. The decisions of managers in this domain set the stage for a company's performance throughout the sales cycle. If they produce a consistently higher quality product or service with larger gross margins than substitutes, the company takes the high ground. Think "Blue Ocean Strategy" when you think of operations management. And remember, Kim and Mauborgne conclude that:

... large R&D budgets are not the key to creating new market space. The key is making the right strategic moves. ... The creation of blue oceans, in other words, is a product of strategy and as such is very much a product of managerial action, not the size or age of the firm (page 5).

A TRIP TO PHILLY

Several years ago a friend of mine was planning a business trip from New Orleans to Philadelphia. Price wasn’t a factor since the company was paying his expenses. Otherwise he might have flown on Southwest Airlines (NYSE: LUV). He decided to book a U.S. Airways (NYSE: LCC) nonstop flight with an upgrade to first class using his Dividend Miles. He went to the website and got the phone number for frequent flyer services because he couldn’t find his account number or password. And he couldn’t remember how many miles he had in his account either.

After punching through several levels of voice screening he waited five minutes listening to recorded messages about how important his call was. He finally got a service rep on the line. He asked her if she would please give him his number and password so he could book an upgrade. Here's the rest of their phone conversation:

“I’m sorry sir we don’t have that information here.”

“What do you mean, isn’t this Dividend Miles?”

“Yes sir, it is. But we don’t keep that information here.”

“Well, where can I get it?”

“You have to call another number, sir.”

“May I have the number?”

“Sir, I don’t have that number here.”

“You don't have that number? This is Dividend Miles for Pete’s sake!”

“Sir, I don’t have that number here.”

“Ok, will you just tell how many miles I have in my account?”

“No sir, I can’t give out that information without an account number.”

“Never mind, I think I won’t fly U.S. Air ever again.”

It turns out he had to fly U.S. Airways anyway because it had the only nonstop flight that arrived in Philly at 2 p.m. in time for his 3:00 meeting. It was the same price as the nonstop Southwest flight. But he didn’t get that first class upgrade and he probably will never get to use his Dividend Miles because he still can’t find his account number and password. So much for their frequent-flyer loyalty program. Next time he says he’ll take Southwest to Philly. By the way, after this experience he sold his shares in U.S. Airways.

The telephone representative did nothing wrong. She couldn’t help it that the company information system she relied on didn’t have the information my friend wanted. Was anyone responsible for his bad brand experience? Yes, enterprise marketing was responsible. Enterprise marketing was responsible for not ensuring that the IT department linked Dividend Miles redemption to membership records.

Can such a small thing hurt the company’s market value? Yes, if it happens to enough customers. How many passengers did U.S. Airways lose every day because of poor brand experiences caused by this “little” slip up? US Airways management didn’t know the answer to this question because they didn’t have that information.

The salary and fringe benefits of the Dividend Miles rep probably were reported in the company's "General & Admiistrative" expense account. Since that's not a "marketing expense" it has no impact on customer or investor perceptions and behavior. Right? Wrong!

Every connection, between every employee and every customer or investor, no matter how seemingly trivial, has an effect on their perceptions and behavior. This is why we must upgrade the role of "marketing" to the enterprise level. What better way to make this happen than to collect all the costs recorded in the accounting system that might affect customer and investor perceptions as "enterprise marketing expenses."

MICROSOFT'S RED, WHITE & BLUE DOLLARS

This graph shows Microsoft's red, white and blue dollars for the year ending June 30, 2006. Enterprise Marketing consisted of three components: R&D expenses (14% of revenues); Sales and Marketing expenses (22% of revenues); and General and Administrative expenses (7% of revenues). These expenses capture the cost of virtually every company driven activity and event that that influences how customers and investors think, feel, and act toward Microsoft during the sales cycle.

Microsoft's earnings before interest, taxes, depreciation and amortization were 36% of revenues. And the cost of revenues was 21%. Want to explore the possibilities for creating new market spaces -- blue oceans? Begin by talking with the folks in operations management.

MAPPING EXPENSES ONTO ASSET BASES

The Statement of General Accounting Standards No. 142 on Goodwill and Intangibles requires that "Costs of internally developing, maintaining, or restoring intangible assets (including goodwill) ... shall be recognized as an expense when incurred (section10, page 10)." In other words, even if these expenses map directly onto the seven asset bases identified in the Harvard Management Update "Getting a Grip on Intangible Assets" they cannot find their way to the balance sheet.

That Harvard Update was based on an unpublished Financial Accounting Standard Baord (FASB) study of the different categories of operating expenses that influence intangible assets. The seven asset bases identified in the study are:

- Workforce-based assets

- Technology-based assets

- Customer-based assets

- Market-based assets

- Organization-based assets

- Contract-based assets

- Statutory-based assets

This table aligns the cost of revenues and Microsoft's enterprise marketing expenses with these seven "asset" bases.

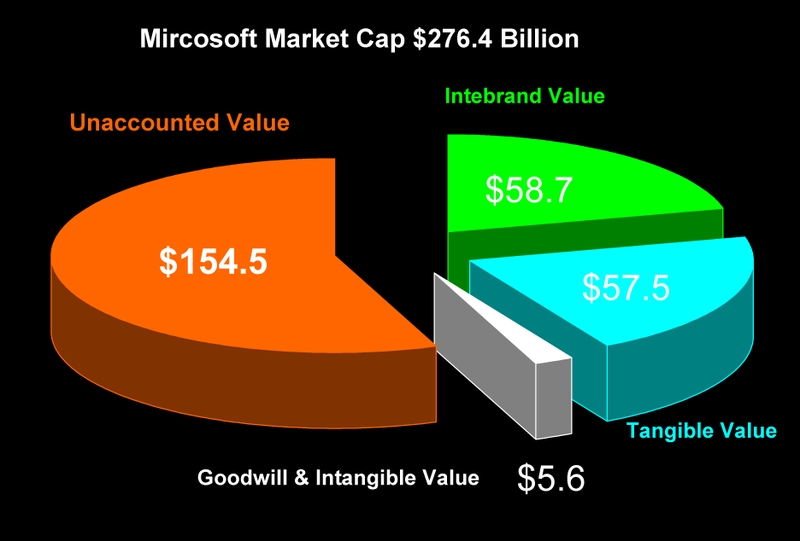

We can map enterprise marketing expenses on six of the seven "asset" bases with which they are associated. R&D expenses contribute to Microsoft's Technological "asset" base. Sales and marketing expenses contribute to its Customer and Market "assets." General and Administrative expenses contribute to Microsoft's organizational, contractual, and statutory "assets." But how do we measure their affect on Microsoft's unaccounted for market capitalization? That is the $154 billion dollar question I asked in the title to the last post in this series.

OPTIMIZING "RED OCEAN" EXPENSES

To begin to answer the question about Microsoft's $154 billion in unaccounted market value we need to compare its actual enterprise marketing "red ocean" expenses with its maximum earnings expenses. If actual expenses exceed those which maximize earnings, the company is throwing money down the drain. If actual expenses fall short of those which maximize earnings the company is leaving money on the table. Either way the market will read the tea leaves and adjust the company's market price accordingly. If Microsoft over-spends on enterprise marketing, that will decrease earnings and depress market value. If the company under-spends on enterprise marketing that too will depress earnings and market value for failing to capitalize on competitors' weaknesses. To maximize shareholder value management must hit the "sweet spot" – the spending level that maximizes earnings.

In 2006 Microsoft management spent $21.9 billion, or 43% of revenues, on enterprise marketing in the management of its "red ocean" expenses. Want to find out if they maximized earnings? Then stay tuned in to this series.

Thanks for viewing.

~V

{kind=link}

{kind=link}

{kind=link}

{kind=link}