When was the last time you were faced with a choice between strategic business alternatives that appeared to be mutually exclusive – "A" or "B" but not both? This seems to be the problem facing The New York Times Co (NYSE: NYT) in searching for ways to monetize its content online. If, however, Mr. Sulzberger were to a look at his choices through the lens of enterprise marketing he might discover "A" and "B" aren't mutually exclusive after all.

What's so special about looking through the lens of enterprise marketing? Two things come to mind. First, an enterprise marketing analysis optimizes the cost of all the expenses that influence how investors, customers, and consumers perceive a company and its products. Second, the competitive risks of a strategy are built into the analysis from the very first right up through the last step.

COMPETING FOR CUSTOMERS AND CAPITAL

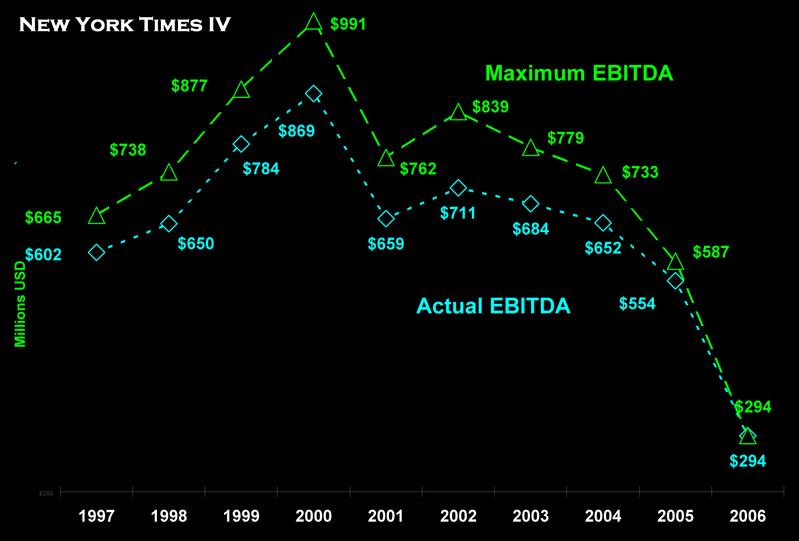

Most economists assume it's not possible to operate as a public trust and -- at the same time -- maximize profits. My last post, "The New York Times Co: Public Trust vs. Maximum Profits," showed that in the case of The Times this assumption did not stand up to the data. The company remained a public trust and maximized profits in 2006. The purpose of this post is to further that conclusion by documenting how a reconciliation of the strategic alternatives faced by The New York Times Co. leads to an EBITDA of $7 a share by 2010. When you consider the company earned just under $2 a share in 2006, hitting this earnings target presents management with no mean feat.

This analysis goes back to the original post in a series on newspapers that began on June 3, 2007 with "Dow Jones: Anomaly or Hidden Value?" In that article I placed The Times in a strategic group with Dow Jones (NYSE: DJ), the Gannett Company Inc. (NYSE: GCI), and the Tribune Company (NYSE: TRB). A strategic group is a set of companies that share a customer base and have comparably deep pockets. In newspapers the “shared customers” are advertisers. This report is based on the same 10 years of financial accounting data I used in that earlier post.

IRRECONCILABLE DIFFERENCES

Anthony Bianco's cover story of Business Week on January 17, 2005 titled "The Future of The New York Times" quotes John Battelle, a co-founder of Wired, with an apparently irreconcilable strategic choice:

The business model that seems to justify the expense of producing quality journalism is the one that isn't growing, and the one that is growing -- the Internet -- isn't producing enough revenue to produce journalism of the same quality.

In the same story he reports that "... disagreement rages within the company over whether NYTimes.com should emulate The Wall Street Journal and begin charging a subscription fee. Undoubtedly, many of the site's 18 million unique monthly visitors would flee if hit with a $39.95 or even a $9.95 monthly charge."

For years management has been working on a product that delivers enough value to sell profitably online. In October 2001 The Times launched the Electronic Edition -- an exact replica of the New York City print edition. I subscribed to it, then let it expire. That version preserved the exact look of the print edition, which was great. But that facsimile format made it very cumbersome to manage on a computer screen. You could zoom in, but then you lost the most of the content. Moving from one page to the next, even on a broadband connection, took a few seconds. You could move only one page at a time, but you couldn't actually turn the page. That edition is still available with these same shortcomings at $14.99 a month. For this post I renewed my subscription. Nothing has changed. You can't even turn a virtual page electronically!

A BIG MISTAKE

If you subscribe to the Sunday Times you probably noticed recently the insert Introducing Times Reader promoting A new way to experience The Times. The Times Reader lacks the look of the electronic facsimile, but it features high level functionality. Like automatic scaling of text and images to fit your screen even when you change font size. And you can move from section to section and back with one click. It does not include some very important stuff from the company's main web site NYTimes.com. All the web logs and interactive features are excluded. Yet this brilliant, if accidental exclusion, completely differentiates the Times Reader.

Apparently management does not hold this view. When you go to the Home Delivery link on NYTimes.com (and enter your ZIP code) you will find the Times Reader is promoted as a "$169 Annual Value ... free to Subscribers." There goes $14.08 a month down the drain. Big mistake!

A DOTCOM BY ANOTHER NAME ISN'T THE SAME

I was raised in a family of newspaper non-readers. Probably because we lived on military bases around the world where home delivery was out of the question. So I never learned to ignore printer's ink on my fingers, the piles of old newspapers, and the uncertainties of home delivery. I never regularly read a newspaper till they created NYTimes.com. For years it's been my home page. While I don't have to put up with the shortcomings of print editions, the NYTimes.com has problems of its own. First, there's the formatting. Enlarge the type face and everything goes out of whack. Second, getting from one section to another requires too many clicks. Third, finding yesterday's news in archives is a pain in the neck. And if older than yesterday's news there's an extra charge.

I happily will keep my subscription to the Sunday Times at $6.50 a pop (I've learned to deal with a newspaper once a week!). And I'll subscribe to the Times Reader at their advertised price of $14.08 a month. I suspect a large percentage of the 18 million unique monthly readers of the NYTimes.com will do the same. If, over time, even 30% of those 18 million monthly visitors subscribe to the Times Reader at $14.08, the income from it will match the $890 million earned from sales of the Times Newspaper in 2006. The 70% who don't, won't know the difference. And ad revenues won't fall because those who subscribe to the Times Reader will still visit NYTimes.com for its blogs and other interactive features. In fact, free of its editorial responsibilities, the NYTimes.com can be enriched with even more interactive features. 3D Cross-Word puzzle anyone?

A good friend of mine loves reading the newspaper: every day, every page, front to back. She loves the printers ink and saves the old papers for other uses. For which she has many as a 2D artist. To her there's also something special about turning the pages. Reminder to Mr. Sulzberger: the Times Newspaper won't go out of style anytime soon.

INVIGORATED INCOME STATEMENT

The financial impact of monetizing The Times high quality content on the Times Reader isn't just volume. It's also gross margin. In 2006 the Times Newspaper had a gross margin of 53.5%, down from 64.5% in 2000. The cost of moving content to the reader probably is very small: maybe 10% at the outside. When the volume of Newspaper and Reader equalizes, combined gross margins will be about 68%.

The following table presents the actual (2006) and Pro Forma (2010) income statements that lead to EBITDA per share of $7, along with the percent changes in each line item.

These results assume strategic group revenue increases at the same modest 3.8% CAGR of the last decade, growing from $18.6 billion in 2006 to $21.6 billion in 2010. Actual market share of 17.7% in 2006 jumps 9 points to maximum earnings market share of 26.7%. The marginal value of a share point increases dramatically as a result of higher gross margins, making it profitable to buy more share points. The effect of modest growth in group revenue combined with a 50% increase in market share drives revenue up 75% from $3.29 to $5.76 billion by 2010. And larger gross margins mean relatively lower costs of production, up just 19%.

The financial impact of this strategy really kicks in with gross operating profits, which increase 124% from $1.760 to $3.936 billion in 2010. The SG&A expenses required to support a 27% market share nearly double. But earnings nearly triple from $294 million to just $1.05 billion. EBITDA per share hits $7 while earnings to revenue double. SG&A to revenue increases only 12%. The Times Reader not only makes NYT much more profitable, it's also more efficient to deliver.

WHAT'S THE NYT PRICE IIN 2010?

A simple way to estimate NYT's price is to multiply its 2006 Price/EBITDA ratio of 12.3 by forecast earnings in 2010. This suggests a price of $87 in current dollars. Remember, that $7 earnings figure assumes management continues to optimize its SG&A expenses every year just as they did in 2006.

The NYT price also is contingent on the actions of competitors. Since Dow Jones soon will be under new leadership, with deeper pockets and an equally powerful brand name, the valuation of NYT must take DJ and its other competitors into account. That's exactly what the competitive stock valuation model in my book Competing for Customer and Capital is designed to do. In the next post in this series I'll apply that model to valuation of the NYT. We'll see if it adds enough information over and above that contained in the P/E ratio to make it worth the extra effort.

The Times Reader solves the problems of both the paper and online editions. It's my ideal product. It also can solve the company's problem of monetizing its content online. The solution is simple: charge separately for The Times Newspaper, Electronic Edition, and Times Reader while keeping the NYTimes.com free.

~V

{kind=link}

{kind=link}

{kind=link}

{kind=link}