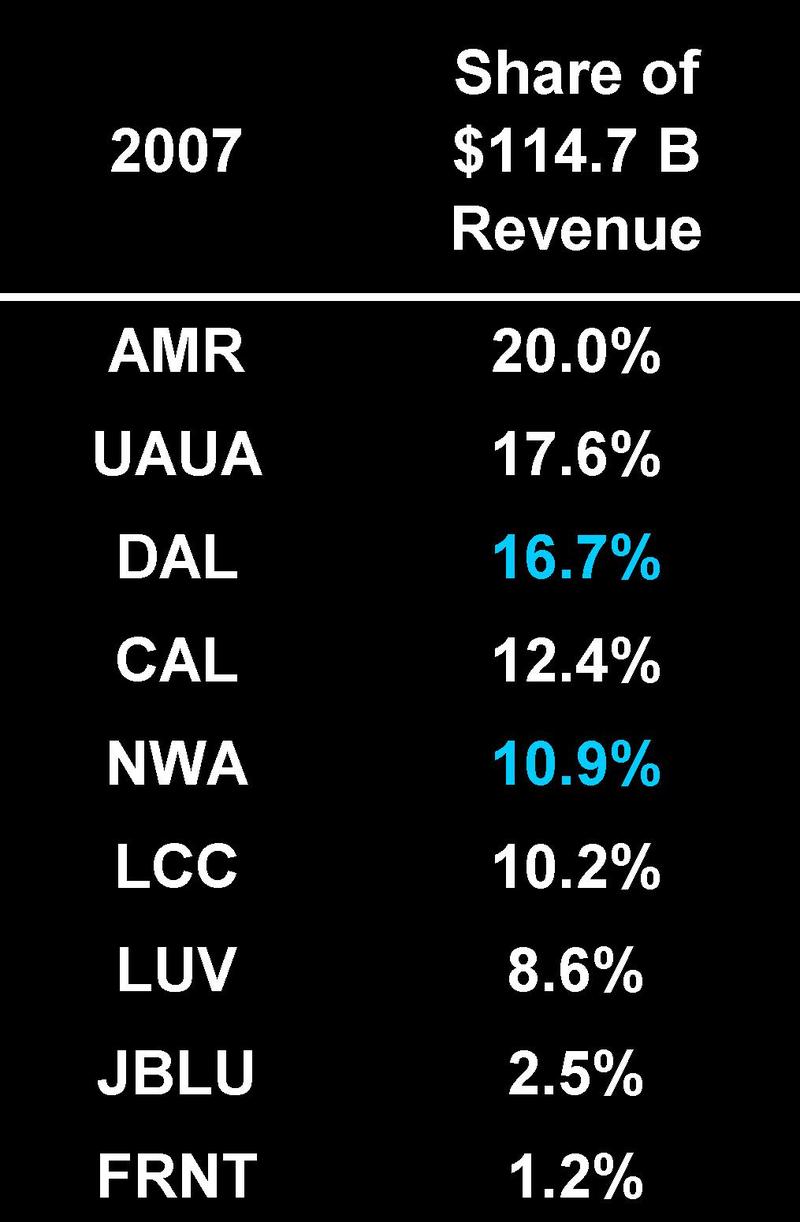

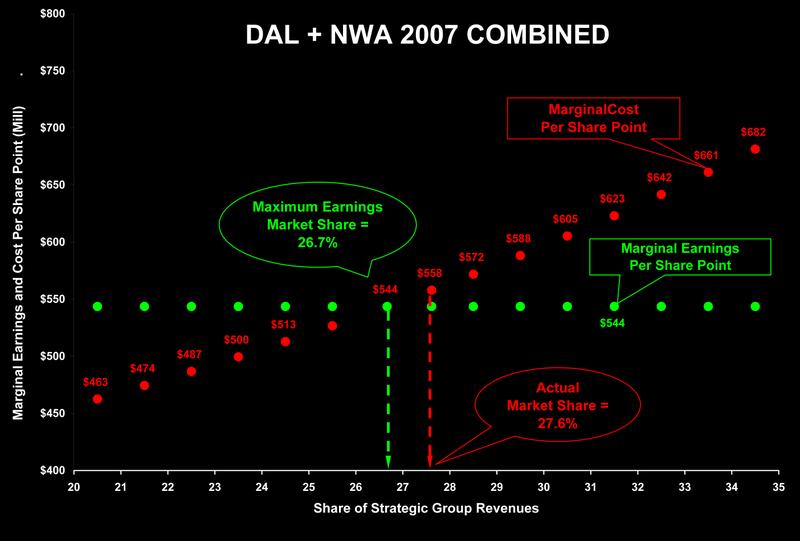

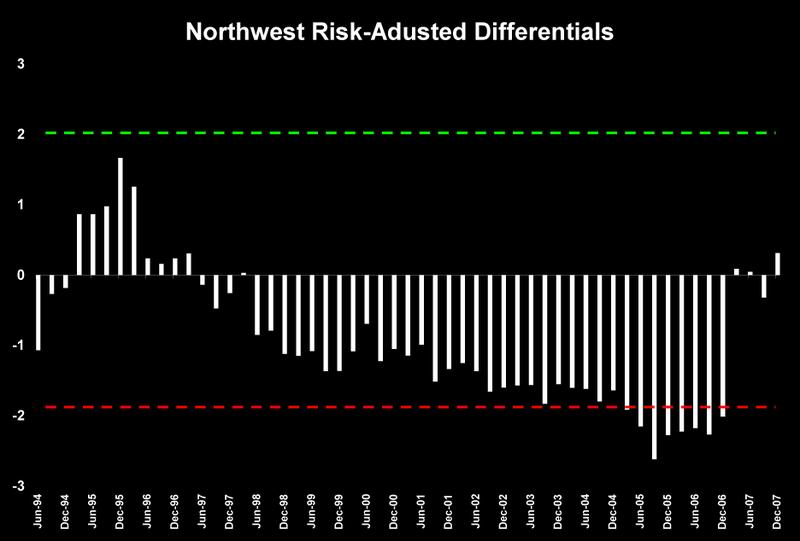

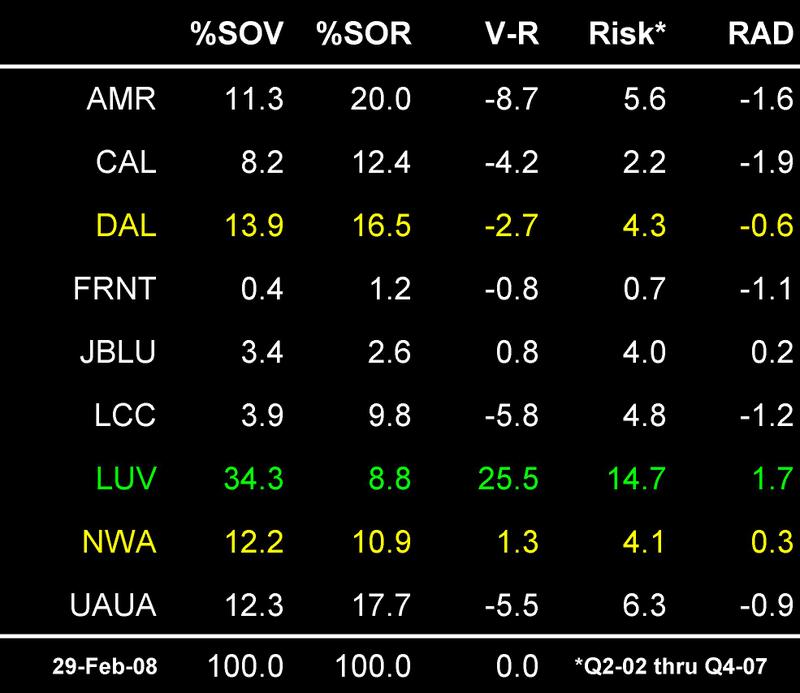

My post on Why Airline Mergers Don’t Work concluded with this double whammy:

Painful price elasticity combines with zero earnings elasticity to squash earnings in the proposed merger between Delta (NYSE: DAL) and Northwest (NYSE: NWA).

The statement was based on the principles in Competing for Customers and Capital, perhaps the only analysis of its kind that could identify this crippling dilemma.

What’s an airline CEO to do in this situation? I recommended they read J.C. Larreche’s book The Momentum Effect for possible cures to what ails them. Here’s what Sir Richard Branson, who knows a thing or two about the airline business, says on the cover jacket:

This book shows you how to build momentum and leave your competitors trailing in your wake.

What might an airline CEO learn from it? I admit, perhaps not the same things I have learned. But here is one insight that jumped from the pages of The Momentum Effect [TME] as I read.

VIBRANT SATISFACTION

The relationship most air carriers have with passengers never develops beyond their onboard experiences, online booking and ticket purchases. As Professor Larrache said:

There is no emotional connection. To generate the momentum effect requires a much deeper and more committed relationship than that offered by passive customers who just don’t complain. Companies should measure their success by the number of delighted customers they have—people so thrilled with a product or service that they can’t help but tell others about it.

Aiming to satisfy customers is not enough. That is an average, complacent, and mediocre goal. Momentum-powered firms are more ambitious in their customer satisfaction objectives. Their target is truly intense, can’t-imagine-any-better satisfaction—vibrant satisfaction (p. 152).

Would offering a non-stop flight in place of a connecting one create vibrant satisfaction? Not really. While non-stop flights are desirable, we’ve all learned to live without them. Finding a non-stop flight is great, but it does not create vibrant satisfaction. A non-stop flight is not something for which you would say: I can’t imagine anything more satisfying in air travel. What sort of air travel service might lead you to express vibrant satisfaction?

WHEN LESS IS MORE

We often hear the idea that “less is more.” But that concept always is expressed in terms of money. The following sentence from TME explains when less is more from the passenger’s point of view:

For [passengers], less should mean that they get exactly what they need and nothing more, with no superfluous elements that create complexity and could destroy value (p.27).

Reading this sentence started me thinking: In my experience are there any airline services that create complexity and destroy value?

SIX TRIPS TO WPB

Two of my sons and grandsons live in West Palm Beach, Florida. So I travel there on a first-class senior fare about six times a year. Currently that fare runs about $1,100 per round-trip. All the flights offered by Continental Airlines (NYSR: CAL) have a plane change in Houston. Usually I check one large suitcase carefully packed with shoes, shirts, sport-coats and several suits surrounding a MacBook Pro wrapped in a towel, plus toiletries packed in plastic bags or snap-tight containers.

I’ve been making this trip on the same CAL connecting flights six times a year for several years. Even so the TSA inspectors take my checked bag apart and throw my suits, shirts, ties, socks and shoes back in wrinkled mess with a little flyer announcing their inspection. As if I couldn’t see they had been there.

THE CURSE OF CHECKED BAGGAGE

On every trip we pay so much attention to our luggage that one might think it mattered more than ourselves. We pack our clothes and toiletries in a suitcase, carry it to the airport, check it and expect the TSA to inspect it. Then we roll it to a taxi or shuttle, take it to a hotel or other venue, unpack and lay out stuff for the next day. And the days after.

Then we replay the process in reverse by returning the clothing and toiletries to our suitcase. We carry it to the airport, check-in for TSA inspection, retrieve it from baggage handling at the end of the flight and take it home to unpack. If it's not lost in handling!

Finally, our local cleaning service picks up the dirty clothes to wash and/or dry clean them. Two days later the service returns the cleaning and we put it put away. There it waits in our dresser for the next trip.

This is an endless, superfluous cycle of baggage handling, and re-handling, and re-re-handling. A cycle of unnecessary complexity that often destroys what ever value might be created by an on-time arrival. Why do first-class airline passengers need to check their baggage? If you think about it, we really don’t. We don’t need “baggage handling” as we know it. What we actually need is another set of clothes and toiletries at our destination.

How could an airline provide another set of clothes and toiletries at a passenger’s destination? By taking on more of the responsibility for them. There are at least two possibilities.

EXPRESS SHIPMENT

Probably the simplest option is for the carrier to partner with FedEx (NYSE: FDX) or UPS (NYSE: UPS) to pick up our baggage from home the day of our departure and deliver it to our destination timed with our flight arrival. With this option our baggage never goes thorough the passenger air transportation system. No baggage to carry to the airport and check-in. No TSA inspection. No waiting at the baggage carrousel to pick it up. Then, just before our return flight, the express service picks up our baggage at the hotel and returns it to our home timed with our arrival.

But this simple solution has one major drawback. It’s simple for the air carrier, but not for the passenger. For example, the express shipment option avoids some of the curses of checked baggage, but not all of them. It's less likely to get lost. But, we still have to pack the suitcase, make an appointment to have it picked up by the express shipper and wait for the truck to arrive. Then on the return trip we have to be home to receive the baggage.

We still must sort the clothing and give it to our cleaning service. Then store it away till the next time we need it. When that day arrives, we must repack the suitcase and wait for the express shipping service to pick it up. We never think of these chores as much of a burden because we always do them. But what if we didn’t need to?

PERSONAL VALET

Another -- far more personal -- option is for the carrier to create a travel partnership with each of its first-class passengers. Roughly speaking, here’s how a personal valet service built on that partnetship might work.

Each partner is issued his or her own Certified Airtravel Valise [CAV]. A coded travel-partner number is etched in the rigid frame of each CAV. Multiple CAVs are available in various sizes and functions (e.g. hanging bag, shoe case).

Initially, travel-partners pack their own set of clothing and toiletries in their valise. Then, before the very first flight with the service, the CAV is picked up by the carrier and stored in a special section of its baggage handling facilities at the local airport. This secure section is dedicated to handling only the airline travel-partners’ baggage. The security must be such that the TSA will approve CAVs as pre-inspected baggage. Securing TSA approval would require careful planning of security safe-guards by the airline.

Whenever the carrier’s first-class travel partner flies to any domestic destination, his or her CAV flies on board the same plane (without inspection) and it is delivered to the hotel or other venue where the passenger is staying. This saves schlepping it from baggage-handling to the taxi and on to the hotel.

On the return trip the CAV is picked up at the hotel by the carrier and loaded on the flight to his or her local airport. Then it's delivered to the passenger’s own valet service where it is dry and/or wet cleaned, repacked in the travel-partners CAV, picked up by the carrier and stored in the private airport lock-up till the next trip. The costs of the cleaning services are billed to the travel partner’s personal account with that vendor. The value of this service will be built into first-class fares for travel partners. This is what JC would call a “power offer.”

EFFECT OF POWER OFFERS

Power offers have a huge effect. First, they create compelling value both for the customer and for the company. Second, a deep emotional engagement drives vibrant satisfaction. Third, a power offer cannot be easily duplicated by a competitor. This leads to higher customer retention levels.

Power offers are a continuous and essential activity in creating and sustaining momentum. As JC describes it:

The accelerating effects of four related components: power offer, vibrant levels of customer satisfaction, retention, and engagement, lend a potent thrust to momentum. These four components support each other in a virtuous circle (p. 151).

EXECUTING A POWER OFFER

It’s easier to define a power offer than to deliver one. What’s required for Continental Airlines to deliver on the promise of a passenger valet service for its first-class passengers? What do you think?

Thanks for visiting. As always, your comments are welcome.

~V

Full disclosure: I recommend this book as a co-author with a long history of collaboration.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}