In Straight From the Gut Jack Welch said “If you’re not #1 or #2, fix it, sell it or close it.” His quote captured the spirit behind the development of the Profit Impact of Marketing Strategy [PIMS] studies by the Marketing Science Institute under the direction of Professor Robert D. Buzzell in the early 1970s. These two works have led nearly every CEO since then to believe that more market share means more profit.

A LITTLE HISTORY

I was the Associate Research Director of MSI in Cambridge, MA in the spring of 1969 when Bob Buzzell cut a deal with Sidney Schoeffler to expand his original study of General Electric divisions on a massive scale. You could say that I was there when PIMS was born. I left for Chicago's GSB that summer.

The PIMS data were used in hundreds of papers published over the next two decades. The first was an HBR article on The Impact of Strategic Planning on Profit Performance by Sidney Schoeffler, Robert D. Buzzell, and Donald F. Heany. A comprehensive review of the entire body of work is available in the PIMS Principles by Bob Buzzell and Bradley Gale published in 1987.

In 1983 I began to study the financial statements of public companies hoping to uncover the “real” relationship between market share and profits. This work culminated in Competing for Customers and Capital published in 2006. That book provides the theoretical underpinnings for these posts. One of the dominant principles is managing market share to optimize earnings. You can get a quick overview of this principle in my audio slide show The Role of Maximum Earnings.

In a nutshell, more market share is a good thing only up to a point. After a company reaches that point, profits begin to decline -- because the cost of the next share point suddenly exceeds it value. Where “that point” occurs depends on a host of things. And it may occur at a very low or a very high market share. But sooner or later that point will be reached.

AIR EXPRESS WARS

In my last post I discussed air express carrier share in relation to their markets for customers as well its equally important relation to the market for capital. The metric I used was the value-sales differential – the difference between each company’s share of value in stock markets and its share of revenue in service markets. For an overview of the theory and properties of this metric see my audio slide show Y'All Buckle That Seatbelt. I concluded the post with these four questions:

- How is UPS able to outperform its peers?

- Why the disappointing results from DHL?

- What left FDX sitting on the bench?

- How can TNT and KNIN move ahead?

One way to explore answers these questions is to consider the degree to which each company managed market share to optimize earnings.

MAXIMUM EARNINGS MARKET SHARE

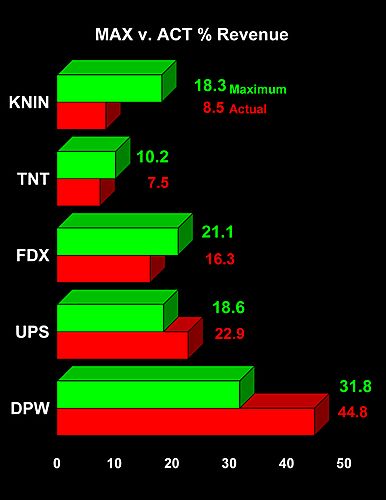

The following chart shows actual and optimal market shares for each of the five leading air express carriers: Kuhne+Nagel (SWX: KNIN); TNT (AEX: TNT); FedEx (NYSE: FDX); United Postal Service (NYSE: UPS); and DHL (XET: DPW).

- DPW turned in the worst performance of the group. Its maximum earnings market share (31.8%) was a full 13 points less than its actual share (44.8%) of revenues.

- UPS turned in a much better relative performance with a maximum earnings share of 18.6% compared with actual share of 22.9%.

- FDX, TNT and KNIN all posted actual shares of revenue that were significantly less than their maximum earnings shares.

OPTIMAL SALES

In ExecEd sessions most CEOs find it a fascinating theoretical exercise to discuss the pros and cons of maximum earnings market share. To them the concept even makes great cocktail party conversation. But when you translate those share numbers into sales revenues the sparks begin to fly!

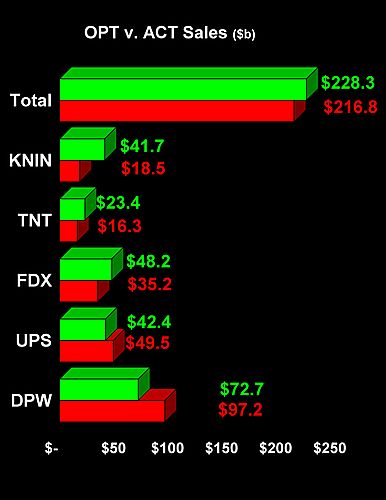

Take the following chart of optimal sales revenues for the top five air express carriers as a case in point. Notice that the combined sales of these companies are close to optimal levels. Actual group sales were $216.8 billion while optimal sales were $228.3 billion. Optimal sales were only 5% greater than actual sales. This is an extraordinary accomplishment for such a complex global industry.

But would you dare tell Dr. Frank Appel that he should plan a sales cut from $97.2 billion to $72.7 billion -- by $24.5 billion USD -- in order to maximize earnings? Would any CEO willingly harvest that many sales for earnings? Sadly, that's what the senior managers of many legacy air passenger carriers are faced with in today’s market.

It might be easier to convince Frederick W. Smith chairman, president and chief executive officer of FDX that he should plan to increase sales from $35.2 to $48.2 billion – about $13 billion – either buy organic growth or through acquisitions.

What do you think Klaus Herms the CEO of KNIN would think about the prospect of increasing sales by 56% from $18.5 to $41.7 billion USD?

OPTIMAL COSTS

Of course all of the strategic recommendations that follow from maximum earnings market share have a dramatic impact on costs. The theoretical results are reported in the following chart.

As you might expect, given the close proximity of optimal to actual group revenues, their combined total operating costs at actual and optimal levels are almost exactly the same – separated by only 1.3% or $2.2 billion USD.

But, again, the picture is very different for DPW. Its optimal operating costs of $48.3 billion were over 62% less than its actual 2007 operating costs of $77.9 billion USD. Even UPS was over-spending in the amount of $7.5 billion or 22%.

FDX was under-spending by $12.1 billion (32%); TNT under-spent by $6.8 billion (33%); and KNIN under-spent by $20.5 billion, or nearly 61%.

OPTIMAL EARNINGS

All of the above brings us to the bottom line – earnings after total operating expenses [EBITD]. The following chart tells the story of actual vs. optimal earnings for each company and the group.

Combined optimal earnings ($53.9 billion) of the five companies were $9.2 billion USD, or 17%, greater than actual earnings of $44.7 billion. The majority of that was accounted for by DPW’s $5.0 billion short-fall.

The company with the most to gain is KNIN. If the company invested in demand to the point that its revenues were optimized it theoretically would increase earnings by 34% from $5.3 to $8.0 billion USD.

COULD IT BE?

If the Chairman of the biggest company in this group might not listen, why bother? Here’s how I look at it. I am writing to plant one seed here and another one there. Hopefully these seeds will grow and eventually a senior manager will listen and consider taking the recommended course of action. Either out of curiosity, when the potential gains are worth the risk. Or out of necessity, when they have no choice. And it really doesn’t matter what the motivation is so long as steps are taken in the right direction.

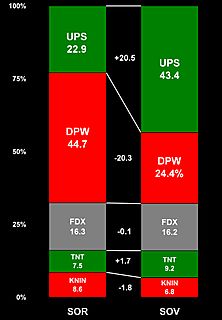

By the way, could it be that the value-sales differential of UPS was +20 points while that of DPW was -20 points partly because its actual earnings were five times closer to optimal than were DPW’s?

Thank you for visiting. As always your comments are welcome.

~V

{kind=link}

{kind=link}