Interbrand's estimate of the 2006 market value of the Microsoft (NASDAQ: MSFT) brand name is $58.7 billion. The value of goodwill and intangibles on Microsoft's balance sheet at the close of its fiscal year on June 30, 2007 was $5.6 billion. The difference of $53.1 billion documents the inability of the company's balance sheet to capture the value of one of its most important market-based assets: the Microsoft brand name. But it does not even begin to reflect what I call the company's "unaccountable." This is the market value that remains unaccounted for after the summation of all "accountable" measures of asset values.

BRAND NAMES IN ENTERPRISE MARKETING

Corporate brands play a much more significant role in enterprise marketing than they do in traditional micromarketing. In fact, much of my book "Competing for Customers and Capital" is dedicated to highlighting the larger role of corporate brands and providing directions on how to deal with it. This is the 6th post in my series designed to document the larger role of corporate brands using real-world, real-time examples backed with published financial data.

The first post in the series was "Sears Brand Bonds," which took a look at how Edward Lampert captured the difference between the book value and the market value of the Sears brand name by issuing brand bonds. The second post applied these ideas to "Coca-Cola's Brand Bonds" to illustrate how the company might create new market value for its 200 lesser known brand names and, at the same time, resolve the ongoing battle with its bottlers. The third took a marketing oriented look at how to create value by co-branding a company's trademark and ticker symbol in Put a Little LUV in Your Logo!. The fourth post on "Brand Value vs. Book Value" was a broad-brush portrayal of the difference between Interbrand values and book values of 49 of the most valuable brands on the planet. My fifth post in the series took this broad-brush analysis a step further by examining the "Interbrand Value vs. Market Cap" of the same 49 valuable brand names. This article focuses on the panoramic view of how all three measures of the value of a company's assets can miss a huge chunk of its market value ... this is what I call the "unaccountable." I picked Microsoft for the analysis because it's the second most valuable brand in the world, after Coca-Cola (NYSE: KO).

MICROSOFT'S ACCOUNTABLES

The three existing measures of the value of a company's assets are (1) the book value of tangible assets, (2) the book value of goodwill and intangible assets, and (3) Interbrand value. In principle all three are what I call "accountables," because the first two already appear on a company's balance sheet and the third may yet find its way there.

Accounting rules that govern the book value of goodwill and intangibles are documented in the Financial Accounting Standards Board [FASB] Statement No. 142 on Goodwill and Intangible Assets issued in June, 2001. A quick take on this one-hundred and ten page document is available in the FASB Summary Statement No. 142.

It's clear from the headline to this post that the Interbrand value of Microsoft's brand name does not appear on its balance sheet. This simple fact provides a glimpse, when it comes to intangibles, of how reluctant financial accountants are to work with all the tools given them by the FASB. Here's what the Board says in its detailed statement on Goodwill and Intangible Assets:

The fair value of an asset (or a liability) is the amount at which that asset (or liability) could be bought (or incurred) or sold (or settled) in a currant transaction between willing parties, that is, other than in a forced or liquidation sale (# 23, page 13).

Since Microsoft is not about to sell its brand name to anyone, that seems to be the end of it. But it's not. On the next page, the FASB statement continues:

If quoted market prices are not available ... A present value technique is often the best available technique with which to estimate the fair market value of a group of net assets (such as a reporting unit). If a present value technique is used to measure fair value, estimates of future cash flows used in that technique shall be consistent with the objective of measuring fair value (# 24, page 14).

This reads like the methodology that Interbrand uses to measure brand value. So, why does Microsoft not take advantage of this option to value its brand name? I don't know the answer to this question. Perhaps some up and coming Microsoft employee does?

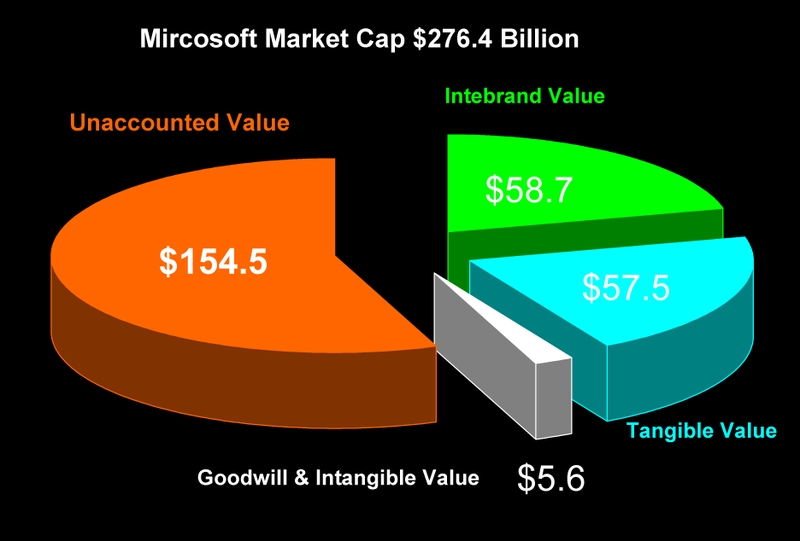

MICROSOFT'S UNACCOUNTABLE

In this chart I divided Microsoft's $276.4 billion market cap into the "accountables" and the "unaccountable." The accountables appear on the right-hand side of the pie. If Microsoft were to use Interbrand's methodology to value its brand name it would appear on the balance sheet as a $58.7 billion intangible asset. Its tangible assets were worth about the same as its brand name, or $57.5 billion. The combined value of the goodwill and intangibles that actually are reported on its balance sheet was $5.6 billion.

If you were to subtract the sum of the accounted for values ($122.9 billion) from Microsoft's market cap ($276.4 billion) you find its unaccounted for value on June 30, 2007 was $154.5 billion.

ACCOUNTING FOR THE UNACCOUNTABLE

Here's Microsoft's $154 billion dollar question: How can you account for the unaccountable? My hope is this post drives home the importance of finding an answer to this question. Fully 56% of Microsoft's market capitalization appears to materialize by magic! And that's only if you include the 21% represented by its Interbrand value.

Is it possible to account for the unaccountable? What do you think?

Thanks for viewing.

~V

{kind=link}

Jonathan,

Thanks once again for your thoughtful comments. Your first point of clarification, that the $5.6bn of disclosed goodwill includes only acquired assets, is sufficiently important that I will add it to the original text.

The second point of clarification, that the accounting profession recognizes only the first two of the three "accountable" assets in my post, begs more answers to the question: Why? I understand you answer: most companies feel that the advantages of putting homegrown brand assets on the balance sheet are outweighed by the disadvantages: explaining the methodology; annual impairment reviews; and the risk of write-downs. But are there not advantages to shareholders beyond the possibility of asset appreciation?

Finally, your suggestion that I look into the importance of each of the seven categories of intangible assets by industry is excellent. In a small way the piece I will post later today moves in that direction. It may come as a surprise that even in a tech driven company like Microsoft, the dollars consumed by sales and marketing begin to approach twice the amount of those consumed by research and development! I definitely will pursue this line of investigation further in coming posts.

~V

Posted by: Victor Cook, Jr., New Orleans, Louisiana | September 30, 2007 at 11:17 AM

Hi Vic

Your latest post continues your tradition of thoughtful, provocative commentary. There are three points that I would like to add - two are points of clarification, and the third is a suggestion for where to focus further analysis.

The first clarification point is that none of the $5.6bn of disclosed intangibles on Microsoft's balance sheet relates to the Microsoft brand (you will remember from my earlier response that disclosed goodwill relates ONLY to acquired assets, not homegrown assets like the Microsoft brand).

The second clarification point is that the accounting profession only recognizes two classes of assets for reporting purposes - tangible assets and disclosed intangibles. There is no general recognition of the Interbrand brand values even though the wording of the FAS rules (141 [dealing with the accounting for goodwill] and 142 [dealing with impairment reviews for goodwill]) appeared to create the opportunity for putting homegrown brands onto the balance sheet. My observation is that most companies feel that the advantages of doing so are outweighed by three disadvantages (having to explain the methodology; having to do annual impairment reviews; and creating the risk of having to do an asset writedown if the valuation shows a decline).

My third point is to reinforce the importance of the task you identify in the final section of your post - how to explain the difference between the observed market value of a company and the value of its physical assets. In your post of September 16 you note that 7 categories of intangible assets have been suggested. How does the importance of each category vary by industry? My guess is that technology is a huge portion of the intangible value of Microsoft but a relatively small proportion of the value of Coke.

Do you have the appetite for an analysis of how intangible value varies by industry sector?

Posted by: Jonathan Knowles | September 28, 2007 at 01:28 AM