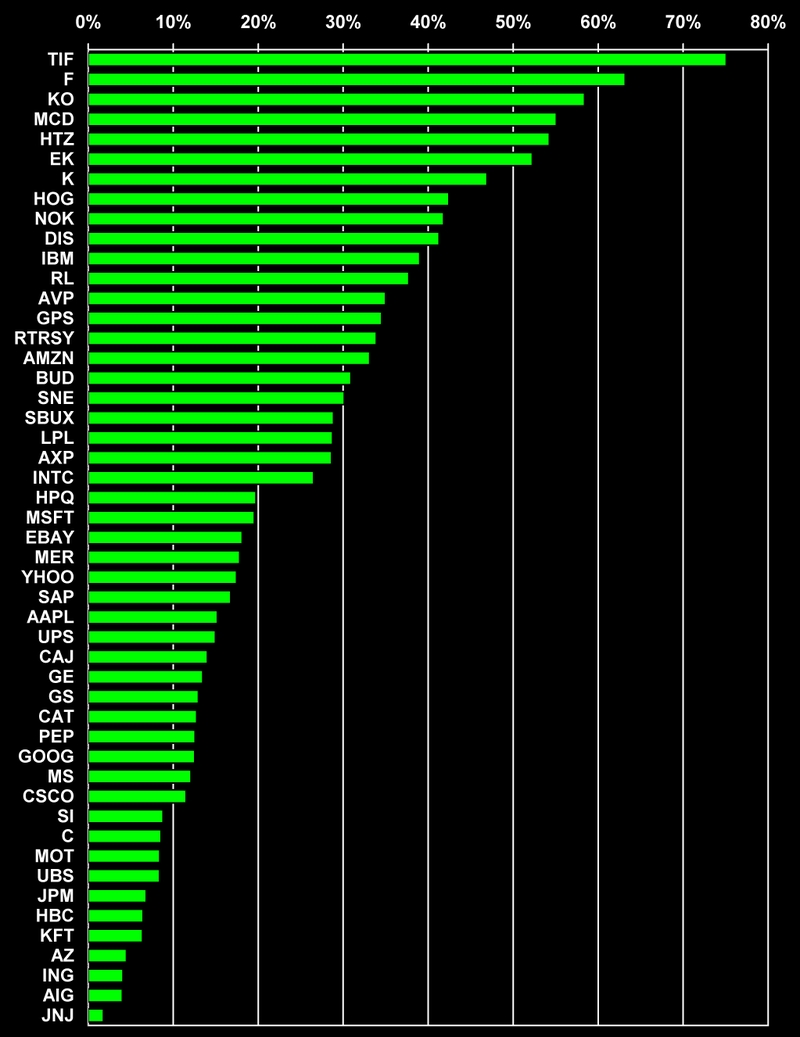

The Interbrand value of Tiffany (NYSE:TIF) is 75% of its $5.3 billion market capitalization. That's no surprise. Tiffany is, above all else, the brand. But the Interbrand value of Johnson & Johnson (NYSE: JNJ) is just 2% of its $191 billion market cap. How do you explain these differences? That's the purpose of this article.

This is the 5th in my series of posts on brands in enterprise marketing. The first, "Sears Brand Bonds," was followed by "Coca-Cola's Brand Bonds." The 3rd article was on "Put a Little LUV in Your Logo!" And last week's was on "Brand Value vs. Book Value." In this post I compare Interbrand valuations with the market capitalization of the same 49 top 100 global brands in their 2007 report. The approach is based in part on an analysis of intangible market value in my book Competing for Customers and Capital.

A FALSE COMPARISON

I've learned at least one thing from posting these blogs: when you get it wrong, someone will let you know! In response to my last post Johathan Knowles, a widely respected consultant whose focus is on the branding dimension of business strategy, had this to say in an email:

I think the whole discipline of relating brand value to some financial metric is laudable - but I think you have chosen the wrong metric. As you know, the accounting regulations only allow for ACQUIRED intangibles to be shown on the balance sheet. The companies with the most disclosed intangibles are therefore those that have done the most - or the largest - acquisitions involving a significant amount of goodwill. It is no surprise that the acquisitive Citi has a low ratio and the non-acquisitive Harley has a stratospherically high one. Comparing overall brand value to disclosed intangibles is therefore a false comparison. The more meaningful question is to analyze what proportion of overall value (and of intangible value) is represented by brands.

Jonathon Knowle's comment motivated me to take a look at brand value and market cap. I think you'll find the results interesting.

A MORE MEANINGFUL COMPARISON

The following chart shows the Interbrand value for each of the 49 top brands as a percent of the company's total market capitalization. Tiffany is at the top of the list with a brand value that is 75% of its market cap. Johnson & Johnson is at the bottom with a brand value that is just 2% of its market cap.

The combined market cap of all 49 brands in 2006 was $4.294 tillion. The combined value of these brands was $735.5 billion. Overall brand values accounted for 17% of market cap. That's not a trivial number. But, I wondered: why the huge difference between Tiffany and J&J? So I ploted the percent of Interbrand value to market cap against the market cap of each company.

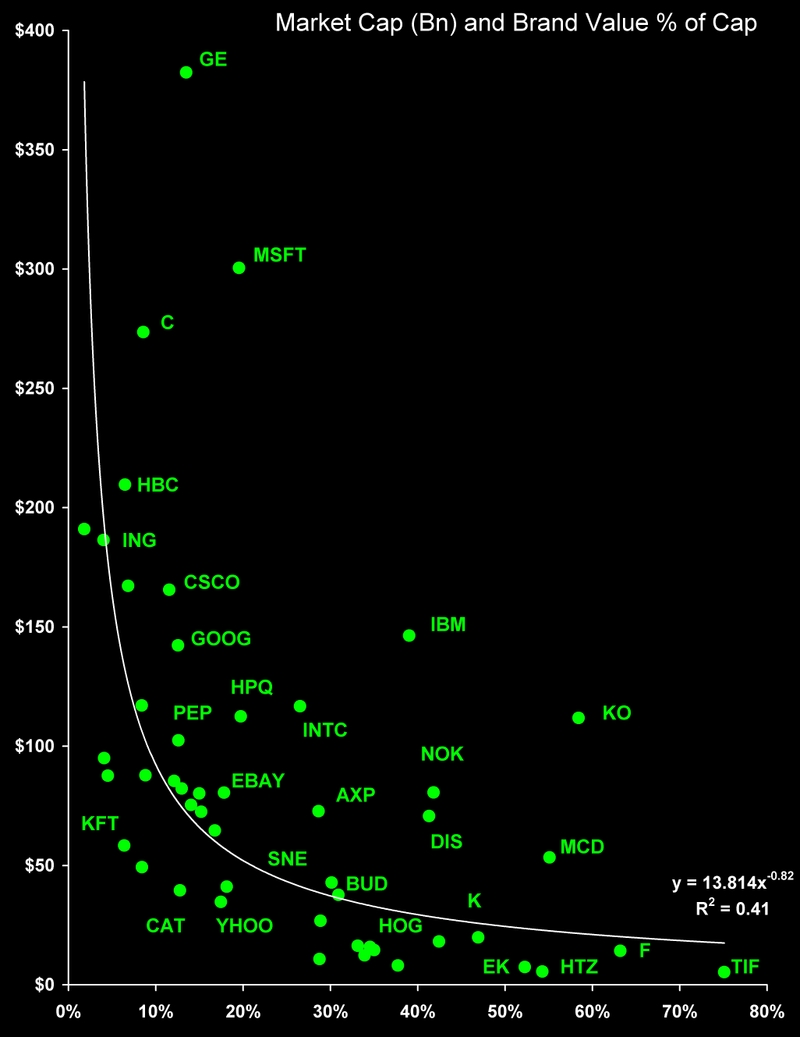

BRAND VALUE DECLINES WITH MARKET CAP

This chart shows how these 49 Interbrand values stand in relation to each company's market cap. Brand value as a percent of market cap declines systematically as company size increases. Market cap in billions appears on the vertical axis, with Interbrand value as a percent of market cap on the horizontal axis.

General Electric (NYSE: GE) is at the top of the chart at 13.5% of its $382 billion cap and Tiffany is at the bottom with 75% of its $5 billion market cap. Microsoft (NASDAQ: MSFT) and Citigroup (NYSE: C) also fit the expected pattern between size and brand value.

FORCES DRIVING INTANGIBLE VALUE

Three powerful forces drive brand values to decline as a percent of market cap: these are company size, market volatility, and other intangibles.

- Company Size: Very big organizations have a lot more going for them than their brand name, even though it may have extraordinary value. GE's Interbrand value of $51.6 billion is just below IBM’s (NYSE: IBM), which makes GE one of the most valuable brands on the planet. But the GE brand is a relatively small (13.5%) part of GE's $382 billion market cap.

- Market Volatility: Interbrand values are long run projections of the present value of cash flows. This makes them less volatile than market values. So, stocks that get beat up in the market will have a higher percentage of capitalization associated with their Interbrand value. Fitting this pattern are Ford (NYSE: F) and Eastman Kodak (NYSE: EK).

- Other Intangibles: The impact of other intangibles on market capitalization is the final and most important factor driving value. The results of an FASB study of these factors were summarized in a Harvard Management Update in 2001: Getting a Grip on Intangible Assets. These are the seven dimensions of intangible shareholder value identified in that study:

> Technology (e.g. R&D)

> Customers (e.g. mailing lists)

> Markets (e.g. brand names)

> Workforce (e.g. management)

> Organizational (e.g. policies)

> Contracts (e.g. royalties)

> Statutory (e.g. patents)

LINKING INTANGIBLES TO MARKET CAP

The fundamental challenge of enterprise marketing is to link spending on these seven intangible drivers to shareholder value. Can it be done? What do you think?

Thanks for visiting.

~V

{kind=link}

{kind=link}

{kind=link}

Jonathan,

Thanks once again for your prompt comment on (and kind words about) this post. I did overlook the "House of Brands" issue. Not because I hadn't thought about it, but because Interbrand methodology published in Business Week says that P&G (and similar companies) were excluded for this very reason. Here's what they say in the BW article:

"Interbrand only ranks the strength of individual brand names, not portfolios of brands, which is why Procter & Gamble (PG ) doesn't show up."

Now, this is no excuse for overlooking the issue, it simply led me to ignore it! Also, the Johnson & Johnson logo appears prominently in all their branded ads. Both in TV and in print the corner of the page rolls open to reveal the JNJ logo and the tag line "A Family Company."

Also notice that Unilever and General Motors no longer appear on the list, but Colgate and VW do. For that matter Coca-Cola has over 200 "individual brands" in its portfolio of beverages. I guess Interbrand's claim to ranking "individual brand names, not portfolios of brands" is open to interpretation. In any event, removing JNJ and KFT from the set won't change the underlying dynamic. Brand value as a percent of market cap drops systematically with company size.

To me, an even more important issue is capturing the impact of the other six forces affecting intangible market value. This is were the biggest gap seems to be, regardless of company size or market volatility. And certainly it is the least explored in marketing, because it requires that we embrace an entirely new perspective on the role of "marketing" in the organization. An "enterprise marketing" perspective. Do you have any thoughts on this issue?

~V

Posted by: Victor Cook, Jr., New Orleans, Louisiana | September 17, 2007 at 03:38 PM

Another really impressive piece of analysis! Thank you for taking my earlier comments on board and for generating this new perpsective so swiftly.

I have one comment to add that may help explain some of your conundrum over the disparate percentage of market capitalization that brand represents for Tiffany (75%) and J&J (2%) - namely that J&J is a multi-brand company whereas Tiffany is a mono-brand company. Your analysis therefore compares the Interbrand value of the J&J brand to the value of its entire portfolio (which includes Band-Aid, Listerine, Neutrogena and Tylenol - plus a vast range of Rx drugs). For it to be an apples-to-apples comparison with Tiffany (which only does business under one brand), we would need to sum the values of all the individual J&J brands and compare that number to the $191 billion number.

This same observation applies to Kraft, P&G, Unilever, Colgate Palmolive and other companies that have a "house of brands" strategy as opposed to a "branded house" strategy. "House of brands" is the dominant model in consumer packaged goods and for certain automotive companies (GM and VW for example).

When this correction is made (and I do not suggest you attempt it as the CPG comapnies have literally hundreds of brands!), my hunch is you would find that the proportion of brand value is close to the level observed for the monobrand companies in consumer industries (such as Disney or McDonalds)

Posted by: Jonathan Knowles | September 17, 2007 at 10:23 AM