Wal*Mart's Mid-Life Crisis: The Secret Solution

In his Business Week cover story "Wal-Mart's Mid-Life Crisis" Anthony Bianco concludes:

… the Arkansas giant's fundamental business problem is that selling for less no longer confers the overwhelming business advantage it once did. Low prices still define the chain's appeal to its best customers, the 45 million mostly low-income Americans who shop its stores frequently and broadly. But the collective purchasing power of these "loyalists," as Wal-Mart calls them, has shriveled in recent years as hourly wages have stagnated and the cost of housing and energy have soared.

He also reports that Wal*Mart stock has dropped 30% below its 2004 high while Morgan Stanley's Retail Index has increased 180%.

THE SECRET SOLUTION

Wal*Mart management began deliberations last year on how to boost the company's sagging stock price. The board's secret report was completed in October, 2006. When early in 2007 a security engineer was fired for releasing some confidential information from that report to the Wall Street Journal a secret solution was revealed:

"The program, called "Project Red," included a consideration of, among other ideas, a possible spinoff of Wal-Mart's Sam's Club warehouse-store unit."

SPIN-OFF SAM'S CLUB?

Here's the question I'm going to answer in this post: Would the sale of Sam's Club bring Wal*Mart close to maximizing its earnings?

The answer is: Yes. It appears that "Project Red" proposed a solution that works. The spin-off would reduce the company's revenue by 27%, increase EBITDA by 66% and bring it within a stone's throw of maximum earnings. This would boost stock price, no matter how Sam's did on its own, and yield cash from the sale to upgrade stores and increase dividends. But before we dig into the details a little background is needed. Starting with the concept of enterprise marketing expenses.

YOU CAN'T SAIL A SHIP FROM THE GALLEY

Marketing is too narrowly defined to deal with strategic issues of which it is a part. "Advertising and promotion" expenses are only a small piece of the marketing challenge. A bigger window is needed to address fundamental marketing questions like those posed by the Sam's Club spin-off.

That bigger window on enterprise marketing expenses is found in Selling, General & Administrative expenses. This is the 800 pound guerrilla of the income statement. All the expenses that drive intangible market value are found in this account. In 2003 over half of Wal*Mart's $229 billion market cap was driven by intangibles (see my paper Marketing Meets Finance Table 4, page 12).

CMOs fail because they are charged with sailing the ship from the galley. You've got to equip the CMO with tools to translate financial concepts into enterprise marketing strategies.

BEING GOOD AT THE WRONG THING ISN'T GOOD AT ALL

Market share is the most widely reported marketing metric in the world. But it's used in the wrong ways: as hindsight instead of foresight; at the segment, but not the enterprise level; as a goal rather than a variable. Market share should be:

• Used to create the future, not just report on the past

• Measured at the enterprise as well as the segment level

• Planned to rise and fall to the level that maximizes earnings

This last point that is critical in understanding the role of enterprise marketing. How exactly do you plan for market share to "rise and fall to the level that maximizes earnings?" It isn't easy, either to calculate or to implement. It requires that management create the future, rather than wait for it to happen.

It turns out Wal*Mart's secret solution offers the perfect opportunity to test my theory of maximum earnings market share. It's as if the board of the biggest enterprise in the country handed me a natural experiment in which to test The Rule of Maximum Earnings! What's this rule? It's surprisingly simple:

SPEND MONEY ON MARKET SHARE UNTIL THE PROFIT FROM ACQUIRING THE LAST SHARE POINT JUST EQUALS ITS COST.

The main reason managers find the result of applying this rule so difficult to accept is too often it points to a significant decline in sales revenues. That's what makes the secret solution proposed in Project Red such an interesting case … the board is considering a $41.6 billion reduction is Wal*Mart's revenues by spinning off Sam's Club. Not because management has run the numbers I'm about to, but because they know their ugly duckling is losing its shoot-out with Costco.

FULL DISCLOSURE

This analysis is based entirely on the theories in my book and 10-K filings with the SEC. I neither have access to management thinking nor inside knowledge about the companies. The results are purely theoretical visualizations of the impact spinning-off Sam's Club would have on Wal*Mart's sales, costs, and earnings in a strategic group with three of its main competitors.

CARVE OUT THE FOREIGN OPERATIONS

Sears Holding Corp, Target Corporation, and Costco Wholesale do not have the same extensive foreign operations that Wal*Mart has. They all have outlets in Canada and Puerto Rico. But Wal*Mart also has many stores in Europe, Mexico, South America, and Asia. The Mexican company's stock (WMMVY) is traded in U.S. markets as an ADR.

To achieve comparability I had to carve out the European, South American, and Asian numbers from Wal*Mart's income statement. Fortunately, the company reports on these operations in sufficient detail to do this with just three assumptions: the ratios of "Cost of Sales" as well as "Operating, Selling, General and Administrative" expenses to revenues are constant across of Wal*Mart's foreign operations and the percent of sales in a country is identical to its percent of worldwide square footage. The company's worldwide sales were $345 billion. Carving out all international sales except Canada and Peurto Rico leaves adjusted sales of $284 billion.

A LOW THRESHOLD AND A HIGH CEILING

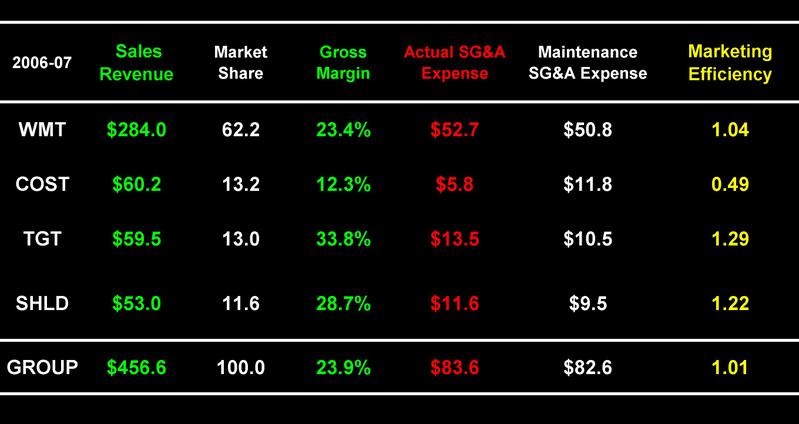

Calculating maximum earnings market share requires only twelve of the numbers in the following table: sales revenue, gross margin and selling, general & administrative (SG&A) expenses for each company. Maximum earnings market share is one of those theories where a few simple calculations (the low threshold) can lead to big discoveries (a high ceiling).

ENTERPRISE MARKET SHARE

Let's begin at the beginning. I use a two year time frame (2006-07) because their fiscal years have different closing dates. The fiscal years of Mal*Mart (WMT) and Sears (SHLD) closed in early 2007 while those of Costco (COST) and Target (TGT) closed in late 2006. The companies generated $456.6 billion in combined sales revenues. Wal*Mart's share was 62.2 percent of group revenues. The market shares of its three competitors were 13.2, 13.0 and 11.6 percent.

ENTERPRISE MARKETING EFFICIENCY

To calculate a company's maximum earnings market share we need a standardized measure of its enterprise marketing efficiency: a metric with an expected value of 1.00. This requirement is met using the ratio of a company's actual SG&A expenses to its market share maintenance SG&A expenses.

In the long run, competition will drive a company to the point where actual and share maintenance SG&A expenses are equal. Very inefficient companies will pull themselves up by their employee's bootstraps through massive layoffs. That's what happened to IBM from 1991 to 2000 (see my audio slide show on The Battle for Your Desktop). Extraordinarily efficient ones will be bested by new business models. That's what Costco did to Wal*Mart: WMT's marketing efficiency is 1.04. COST's marketing efficiency is 0.49. This means that COST is paying just $0.49 for SG&A resources that cost WMT, TGT and SHLD $1.04, $1.29, and $1.22 respectively. This finding holds generally even though Costco's definition of SG&A expenses excludes warehouse and transportation costs while Mal*Mart includes them. For a short discussion of what's behind these numbers see my audio slide show "In Search of Maximum Earnings" beginning with slide number 7 "The Sundown Rule."

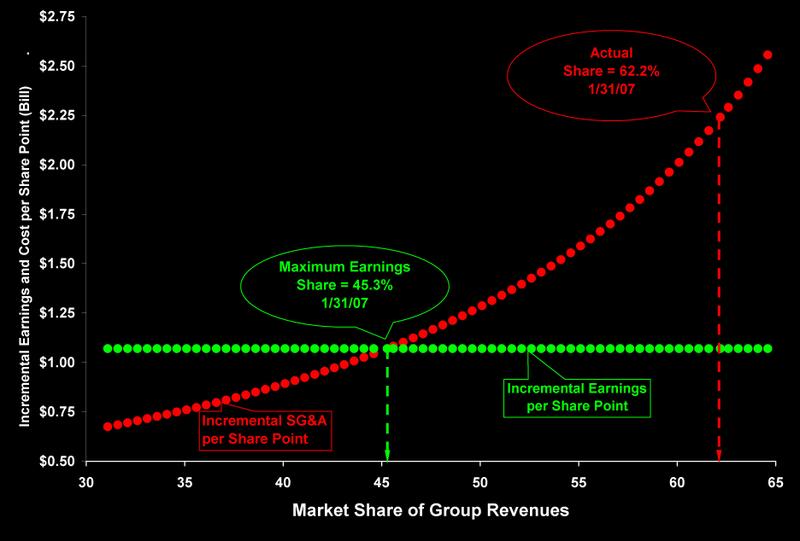

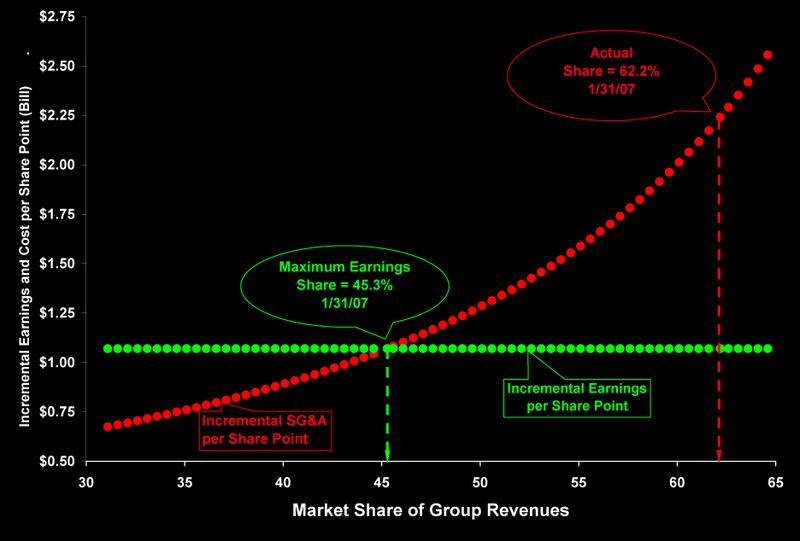

MONEY DOWN THE DRAIN

Wal*Mart's incremental cost per share point (the upward sloping red curve in the following chart) was $2.24 billion. Its incremental earnings per share point (the flat green schedule) were just $1.07 billion. To hold on to that 62nd share point the company threw $1.2 billion down the drain in 2006. The rule of maximum earnings states that:

WMT SHOULD DECREASE SG&A EXPENSES UNTIL EARNINGS FROM THE LAST SHARE POINT EQUAL ITS COST.

Wal*Mart's incremental SG&A expenses equal its incremental earnings per share point at 45.3 percent of group revenues.

How can this be? It goes right back to the fundamental problem cited in the Business Week story: "… selling for less no longer confers the overwhelming business advantage it once did." Their margins are too thin relative to their competitors. This is due partly to Sam's Club and partly to its failure to attract middle class consumers without alienating its loyal low-income shoppers.

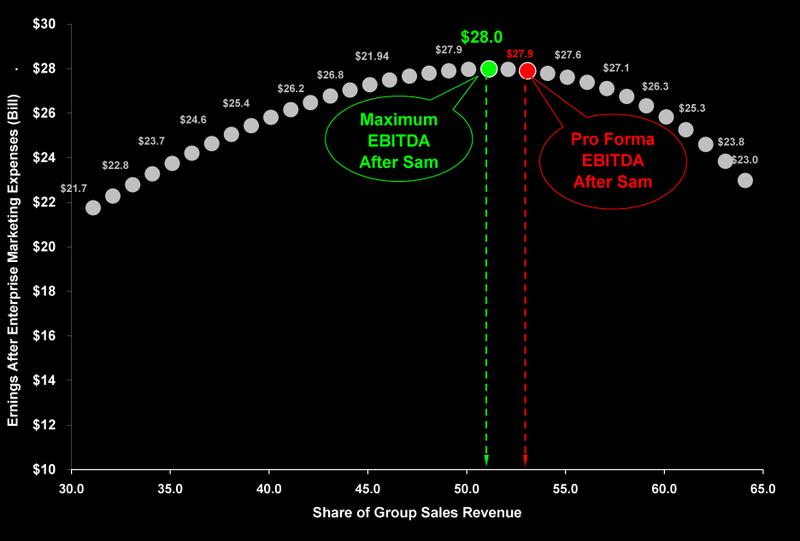

PROJECT RED WINS

The next chart tells the story of the secret solution. If management spins-off Sam's Club they would jettison $41.6 billion in revenues and a big chunk of SG&A expenses. Sam's would become the 5th free-standing player in the space and Wal*Mart's share of group revenues would fall to 53.1 percent. Its SG&A expenses should decrease to around $36 billion and enterprise marketing efficiency should increase to 0.83, resulting in an increase in EBITDA from its current $17 to $28 billion. The company's maximum earnings market share in this reconfigured space is 50.4 percent.

BINGO!

WMT's stock price pops and they pocket cash from the sale of Sam's Club to payout in dividends and upgrade existing stores. A virtuous circle is in place. And the beauty of the "secret solution" is that management isn't cutting revenues, they're just maximizing earnings!

~V

Great finds

- Casino Italiani Non Aams

- Nuovi Siti Casino

- Casinos Not On Gamstop

- Casinos Not On Gamstop

- Casino Sites Not On Gamstop

- Casino Online Non Aams

- Casino Online Non Aams

- Casino Sites Not On Gamstop

- Best Casinos Not On Gamstop

- Sites Not On Gamstop

- Non Gamstop Casinos UK

- Best Non Gamstop Casinos

- Non Gamstop Casinos UK

- Casino Sites Not On Gamstop

- UK Casino Sites Not On Gamstop

- UK Online Casinos Not On Gamstop

- Non Gamstop Casino

- UK Online Casinos Not On Gamstop

- Sites Not On Gamstop

- Non Gamstop Casinos

- Non Gamstop Casino Sites UK

- Non Gamstop Casinos UK

- Casinos Not On Gamstop

- Casino Non Aams Sicuri

- Casino Not On Gamstop

- Casino Online

- Meilleur Casino En Ligne Français

- Nouveau Casino Belge En Ligne

- I Migliori Casino Non Aams

- Casinos En Ligne France

- Casino En Ligne France

- Paris Sportif Ufc France

- топ крипто казино

- Miglior Sito Casino Online

- Casino En Ligne Qui Paye Vraiment

- Migliori Casino Online Italia

- Site Casino En Ligne

- Meilleurs Casino En Ligne

- Tortuga Casino

- Casino En Ligne

- Casinos En Ligne

- Casino En Ligne Argent Réel

- Casino En Ligne Retrait Immédiat

- Casino En Ligne

{kind=link}

{kind=link}

{kind=link}

{kind=link}