Google vs. Microsoft: Crossing the Bule-Ocean, Red-Ocean Divide

Between the 1st and the 2nd calendar quarters of 2007 Google's sales (NASDAQ: GOOG) increased from $3.664 to $3.872 billion. That's nearly 6%. In the same period Microsoft's sales (NASDAQ: MSFT) decreased from $14.398 to $13.371 billion. That's a decline of over 7%. And it's the only time in the last ten quarters that MSFT experienced a March to June quarterly decline in revenues.

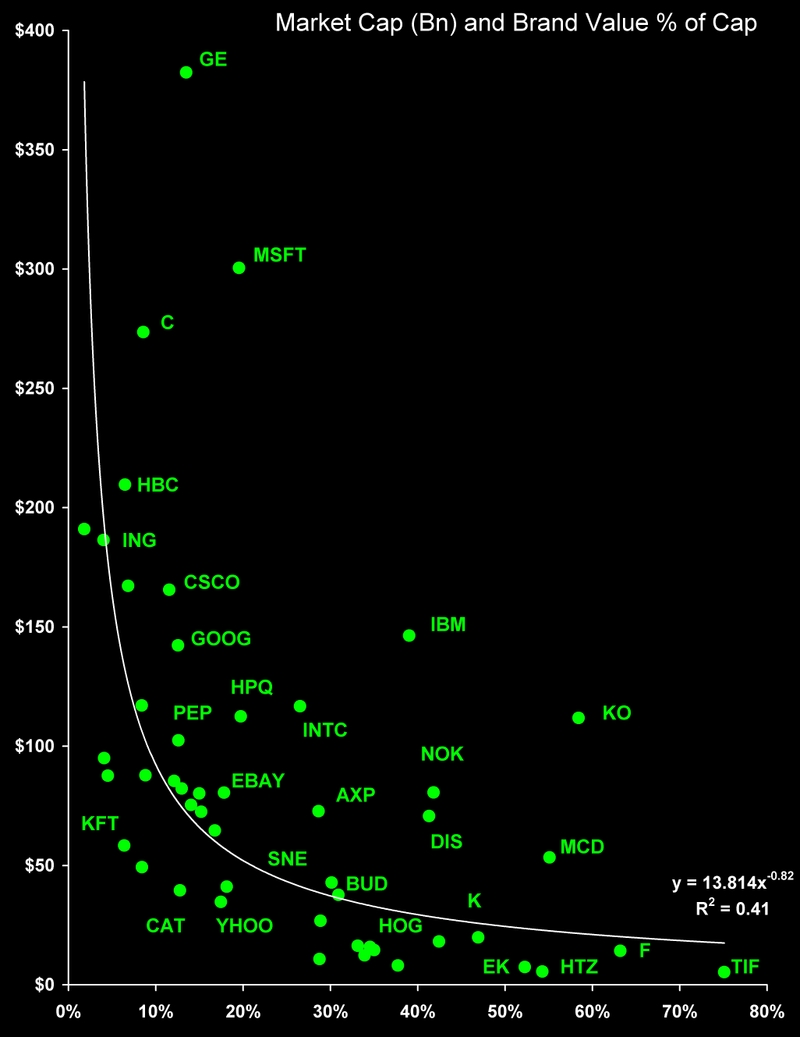

From March 30 to October 19, 2007 Google's market cap increased over 42% from $142.2 to $201.2 billion. In that same period Microsoft's market cap increased just a bit over 8% from $261.4 to $283.0 billion.

It's a common expectation that when one company's revenues increase at the same time as a rival's revenue declines, both stock prices will be affected. This is an expectation one could easily forget while tracking the valuation measures currently reported in popular financial services like Yahoo!. Why? Because implicitly these measures assume that companies operate in a blue ocean – that they have no competitors.

Pick any popular metrics you want, from Price/Earnings to Market Cap or Enterprise Value to Earnings. They all are completely company specific. They do not even hint at how the 6% increase in Google's revenues, coupled with the 7% decline in those of Microsoft, might affect their respective market caps in the next quarter. Why? Because we seem to think it's all a mystery. Well, it isn't a mystery any longer. In my book Competing for Customers and Capital I pull back the curtain to reveal the often subtle and complex relationships between the sales revenue and market value of competitors.

SOME BACKGROUND

This is the 4th in my series of posts on the competition between a blue-ocean superstar (Google) and its red-ocean rival (Microsoft). This one, like the earlier posts in the series, was inspired by Blue Ocean Strategy, the book by Professors Kim and Mauborgne of the INSEAD business school in Fontainebleau, France.

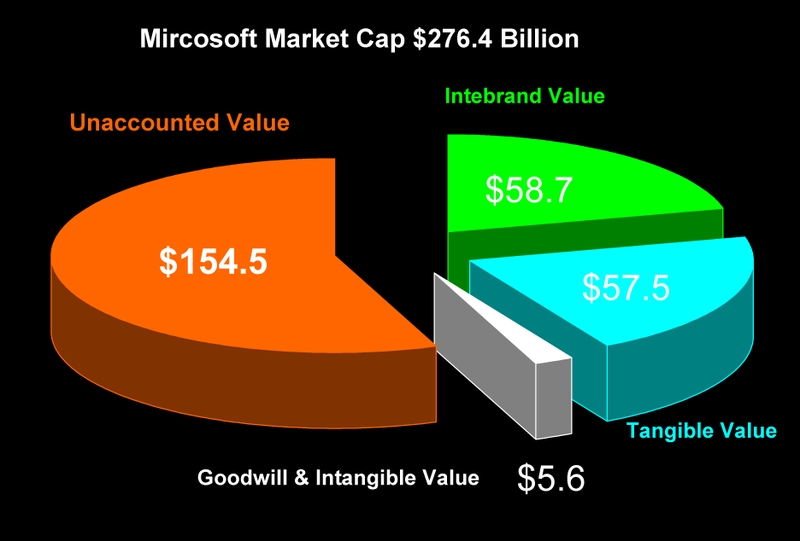

The 1st post in this series was "Microsoft's $154 Billion Question: Optimizing Red Ocean Expenses." In it I mapped enterprise marketing expenses onto the sources of intangible market value and introduced a simple measure of how shareholders know if they're are getting their money's worth from "red ocean" spending. In the 2nd post on "Microsoft vs. Google: The Battle for Your Network" I argued that however appealing blue oceans may be, nearly every company ends up in a sea of red ocean expenses. At that point the most compelling question is how to manage expenses in this environment. Theoretically, the best way to do this is to "optimize" these costs. The 3rd post in the series was "Google vs. Microsoft: Blue vs. Red Ocean Earnings Productivity." That one addressed a larger question: are there significant differences between the earnings productivity of "Blue Ocean" compared with "Red Ocean" companies? The short answer is, yes at least in the case I am currently reviewing.

A SURPRISINGLY SIMPLE TRANSFORMATION

Here is a surprisingly simple transformation of commonplace financial accounting data into a metric that captures the competitive interactions between the separate, but equally important, markets for customers and capital. I call it the risk-adjusted (value-sales) differential: RAD (with a short "A"). It's what you need to cross the blue-ocean, red-ocean divide.

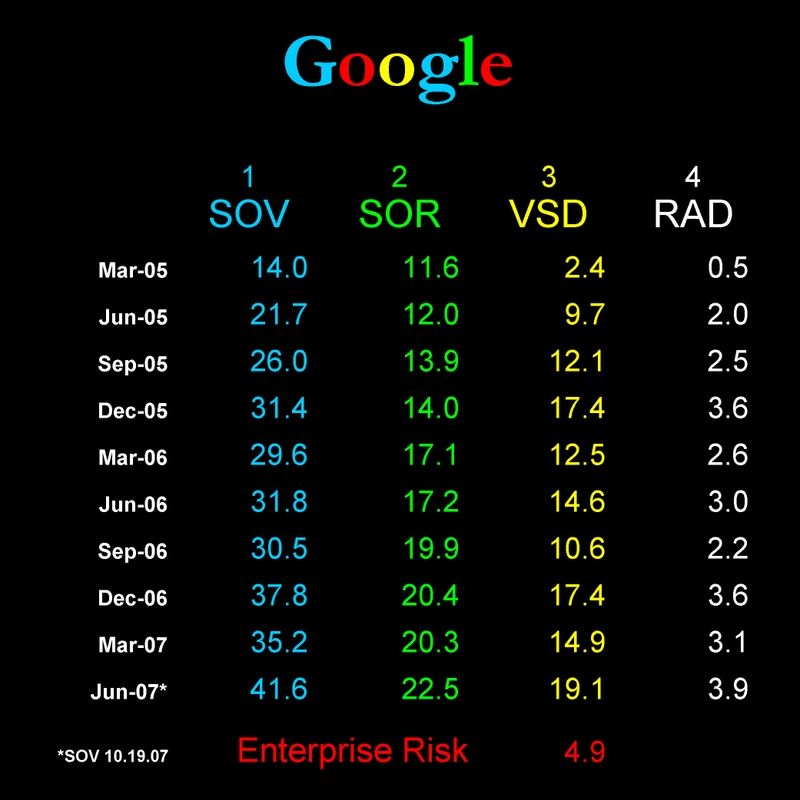

Column 1 in this table shows Google's share of value (SOV) based on the closing price of its stock at the end of each quarter from March 2005 through the close of trading on October 19, 2007. Column 2 shows the company's share of revenue (SOR) from March 2005 through June 2007. Quarterly value-sales differentials (VSD = SOV-SOR) appear in column 3. Enterprise Risk, the standard deviation in Google's VSDs, was 4.9. Risk-adjusted differentials in column 4 equal VSD/Risk. These ranged from a low of 0.5 in March 2005 to a high of 3.9 last Friday (using June 2007 revenue numbers for both companies). When Microsoft files its latest quarterly report with the SEC on October 25 I'll update the revenue numbers for both companies.

CROSSING THE DIVIDE

From a technical point of view, applying the RAD metric to a company produces a standard normal variable (mean zero and standard deviation one). Practically speaking, RAD captures the competitive interactions between sales revenue and market value.

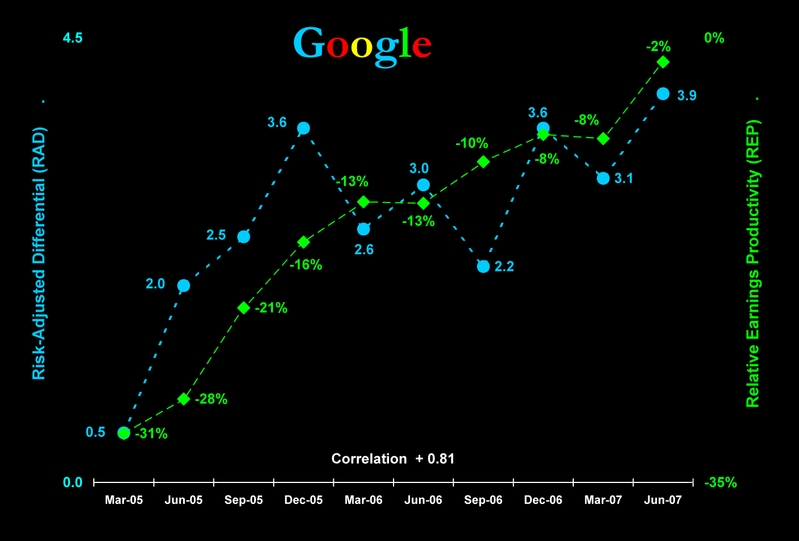

In the following chart risk-adjusted differentials are on the vertical axis ranging from +5 to -5. The 95% confidence limits within this range are marked by the dotted lines at +2 and -2 RADs. Ten quarters, marked by their month's end, appear on the horizontal axis.

With only two companies, risk-adjusted differentials always will be mirror images of each other. Notice that with the exception of March 2005, all of Google's differentials are greater than +2.0, meaning they are statistically significant at a 95% confidence level. Besides the March quarter all of Microsoft's differentials are less than -2.0 at the same confidence level.

The meaning of this chart is simple, yet powerful. In the last nine of the ten quarters since Google went public investors rewarded management with a significant value premium over and above its market power – the company captured only 22% of combined revenues, but created 42% of combined value. Of course, it follows that investors punished Microsoft by discounting its value relative to its market power. The company captured 78% of sales revenues, but created only 58% of shareholder value. In the long run, this is how free markets deal with monopolists.

ON THE OTHER SIDE OF THE DIVIDE

The best part of this story is what you see on the other side of the blue-ocean, red-ocean divide ... when both capital and customer markets are firing on all twelve cylinders.

The two axes on the following chart combine Google's earnings productivity (from my last post) with its risk-adjusted differentials. Risk-adjusted differentials [RAD] are calibrated on the left-hand blue axis from 0.0 to +4.5. Relative earnings productivity [REP with a short "E"] is calibrated on the right-hand green axis from 0% to -35%. REP is the ratio of actual to maximum potential earnings scaled to equal zero when they are equal.

In the 1st quarter of 2005 Google's actual earnings [EBITDA] fell short of its theoretical maximum by 31%. Theoretical maximum earnings are the point at which outgoing costs equal incoming profits, at the margin. Over the next nine quarters Google management guided the company systematically in the direction of greater relative earnings productivity. By June of 2007 the difference between actual and maximum earnings was just 2%. Over the same period Google's risk-adjusted differential increased more or less systematically from +0.5 to +3.9 points. The correlation between the two is +0.81.

By now you may be wondering what Microsoft looks like on the other side of the divide. The next chart tells its story using the same language. And it's not a pretty picture.

Microsoft's risk-adjusted differentials are the mirror image of Google's. But the company's relative earnings productivity is dramatically different. In March 2005 Microsoft's actual earnings after all expenses fell 42% short of its theoretical maximum. And the pattern didn't improve much over the next nine quarters. Microsoft's relative earnings productivity followed a zigzag path reaching a high of -18% in March 2007 and closing the last quarter at -36%. The correlation between Microsoft's risk-adjusted differentials and relative earnings productivity is -0.21. Beginning in March 2006 the two more or less move in step.

WHY DO THESE METRICS MOVE TOGETHER?

My RAD and REP metrics are not currently used by investors to value a company's stock. So why do they move together? Can it be that theses metrics capture underlying, but otherwise unobservable and mysterious, market behavior? Or is it simply that Google, on the blue-ocean side of the divide in this market, is in the driver's seat? Motivating investors' performance expectations on revenues, earnings and market value to follow its lead in the competition with Microsoft, on the red-ocean side of the divide?

Whatever the reasons, I believe these metrics pull back the curtain on market mysteries enough to consult them in forecasting stock prices. To find out how to do just that, stay tuned to this station. Next week, after Microsoft releases its September quarterly report (providing a full deck of fresh, concurrent information on both companies) I'll forecast their closing stock prices on Monday December 31, 2008.

Thanks for viewing.

~V

Great finds

- Casino Italiani Non Aams

- Nuovi Siti Casino

- Casinos Not On Gamstop

- Casinos Not On Gamstop

- Casino Sites Not On Gamstop

- Casino Online Non Aams

- Casino Online Non Aams

- Casino Sites Not On Gamstop

- Best Casinos Not On Gamstop

- Sites Not On Gamstop

- Non Gamstop Casinos UK

- Best Non Gamstop Casinos

- Non Gamstop Casinos UK

- Casino Sites Not On Gamstop

- UK Casino Sites Not On Gamstop

- UK Online Casinos Not On Gamstop

- Non Gamstop Casino

- UK Online Casinos Not On Gamstop

- Sites Not On Gamstop

- Non Gamstop Casinos

- Non Gamstop Casino Sites UK

- Non Gamstop Casinos UK

- Casinos Not On Gamstop

- Casino Non Aams Sicuri

- Casino Not On Gamstop

- Casino Online

- Meilleur Casino En Ligne Français

- Nouveau Casino Belge En Ligne

- I Migliori Casino Non Aams

- Casinos En Ligne France

- Casino En Ligne France

- Paris Sportif Ufc France

- топ крипто казино

- Miglior Sito Casino Online

- Casino En Ligne Qui Paye Vraiment

- Migliori Casino Online Italia

- Site Casino En Ligne

- Meilleurs Casino En Ligne

- Tortuga Casino

- Casino En Ligne

- Casinos En Ligne

- Casino En Ligne Argent Réel

- Casino En Ligne Retrait Immédiat

- Casino En Ligne

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}