Reconsidering Citigroup: The Middle Line and 3D Marketing

Does an investment bank need to be as big as Citigroup (NYSE: C) to be as efficient? No. In the most recent quarter, Lehman Brothers (NYSE: LEH), at just one-third the size, had lower enterprise marketing expenses per dollar revenue than Citigroup. Do risk-adjusted differentials change with strategic group membership? Yes. The numbers change, but trends and rank orders don't.

SUMMARY OF 1st POST IN THIS SERIES

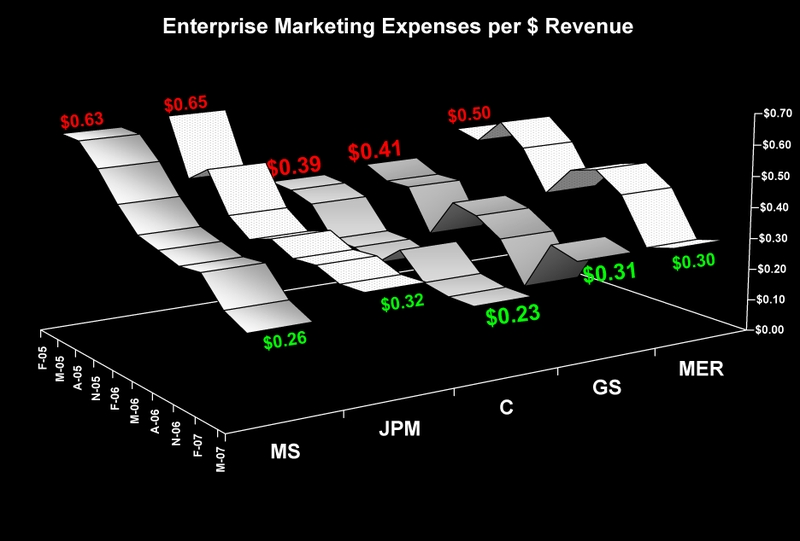

In "Citigroup's Enterprise Marketing Expenses: The Middle Line" I compared the company's enterprise marketing cost per dollar of revenue with four competitors. Citi reported the lowest of them all: just $0.23 in March, 2007. Morgan Stanley (NYSE: MS) was the runner-up with a CPD of $0.26 in May, 2007.

Over the ten most recent reporting periods the CPD numbers for Citigroup and Morgan Stanley dropped dramatically from $0.39 and $0.63 respectively. In the same reporting periods J. P. Morgan's (NYSE: JPM) fell from $0.65 to $0.32; Goldman Sachs (NYSE: GS) declined from $0.41 to $0.31; and Merrill Lynch (NYSE: MER) went from $0.50 to $0.30. A lot of belt tightening was going on in this strategic group.

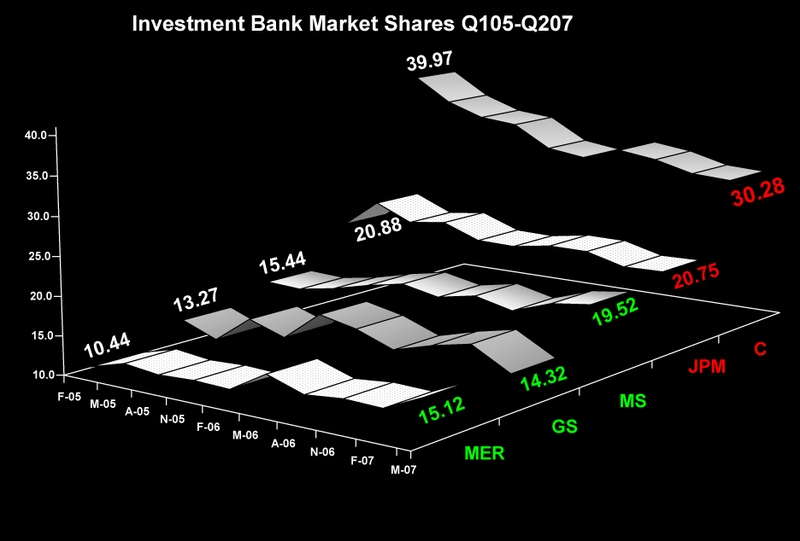

In the same post I found that Citigroup's 40% share of revenues in March, 2005 was almost double that of JPM 's weak second place 21% share of revenues. I speculated there may be scale economies in Citi's enterprise marketing cost per dollar.

SUMMARY OF 2nd POST IN THE SERIES

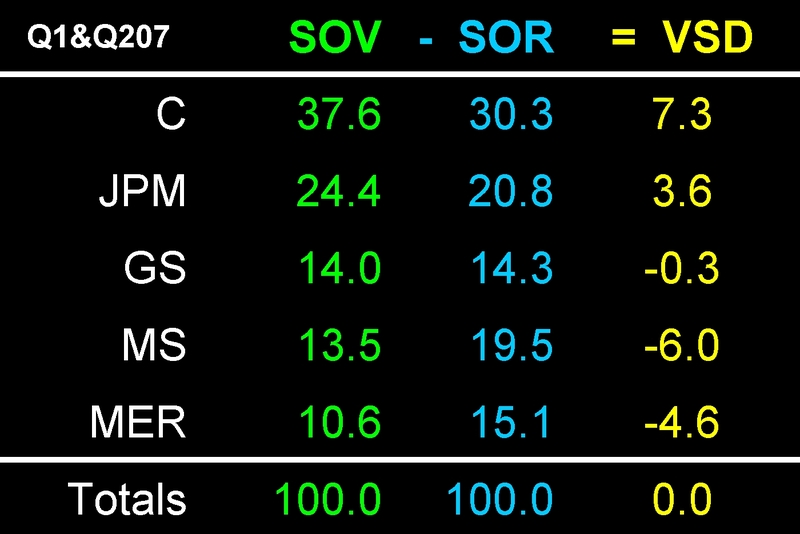

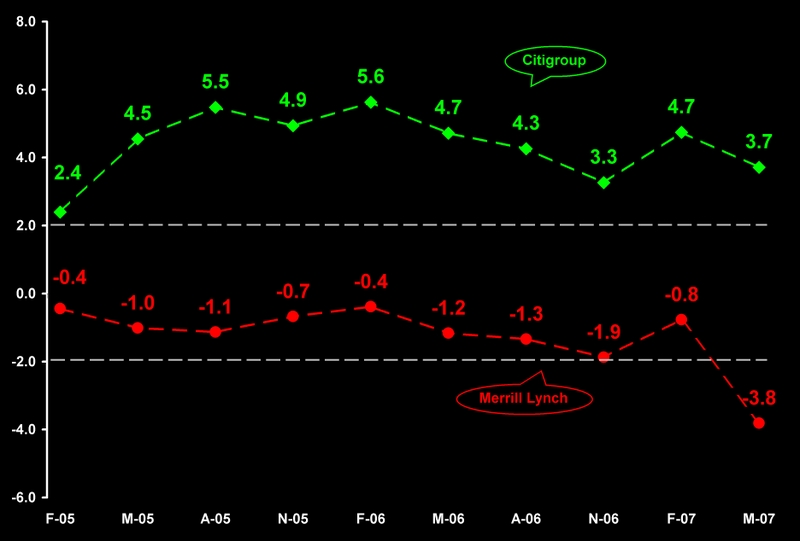

In "Citigroup's Differentials: 3D Marketing Metrics" I compared the risk-adjusted differentials of the five companies. Again, Citi won hands down with a differential of +3.7 in March, 2007. Citi's differential was a standard deviation of 3.7 above the expected value (zero). Merrill Lynch earned a risk-adjusted differential of -3.8. Or, MER's differential was 3.8 points below the expectation. What does this mean? In this strategic group Citi's risk-adjusted value creation was 3.7 times its revenue churn. Merrill's revenue churn was 3.8 times its value creation.

These two posts were visited several hundred times. One viewer spent 12 seconds on my site. It's safe to say he or she wasn't at all interested. Another viewer spent 80 minutes on the site. It's safe to say he or she was very interested. In fact one of the viewers, using the pseudonym "Veryinterested," posted a series of thoughtful comments regarding these two questions:

- Does Citigroup belong in this strategic group?

- What happens if Citigroup is removed?

MARKETING'S MYOPIA

The greatest roadblock to understanding enterprise marketing was planted in the mind of business school students by marketing professors ... including myself. Our micro-marketing perspective asserted that only brands compete. And then, only if they serve the same customers, fulfill the same needs, and deliver the same solutions, in the same geographic market segment. Marketing's myopia has led almost everyone here to believe you must drill down to the geographic market segment to conduct a proper competitive analysis.

STRATEGIC GROUP THEORY

Fortunately, there are countervailing points of view that offset micro-marketing's myopia. One of these of course is Michael Porters "Competitive Strategy." His "five forces model" is enterprise based. A second countervailing point of view is found in the literature of business strategy. There you will find the concept of "strategic groups." Theoretically, companies are direct competitors within a strategic group if they have (or might acquire) a high degree of "market commonality" and "resource equivalence." If you're interested in the details, see the 11 minute Adobe Connect presentation "Who's in My Strategic Group?"

A trade-off between "shared customers" and "deep pockets" is involved in the definition of a strategic group. In the broadest sense, every firm is in competition with all other firms in its competition for capital; however, a limit is imposed by the requirement for some level of current (or anticipated) product market commonality. Otherwise, we lose an important dimension of the competitive effects (shared customers) embedded in a strategic group.

What does this mean in practical terms? If the companies in a strategic group currently do (or might in the future) share a lot of customers and have similarly deep pockets they are direct competitors. Using these criteria the five investment banks in the first two posts in this series can properly be treated as direct competitors. Many others also might also be included as either "potential" or as "indirect competitors;" among them are European and Asian banks.

LEHMAN'S MIDDLE LINE

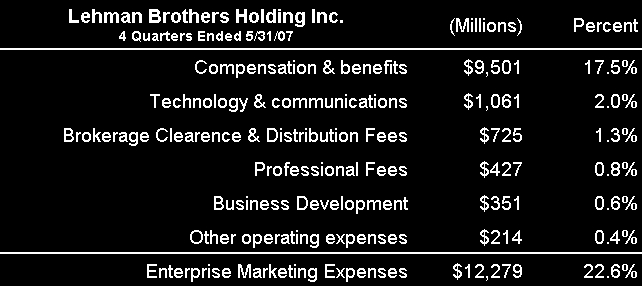

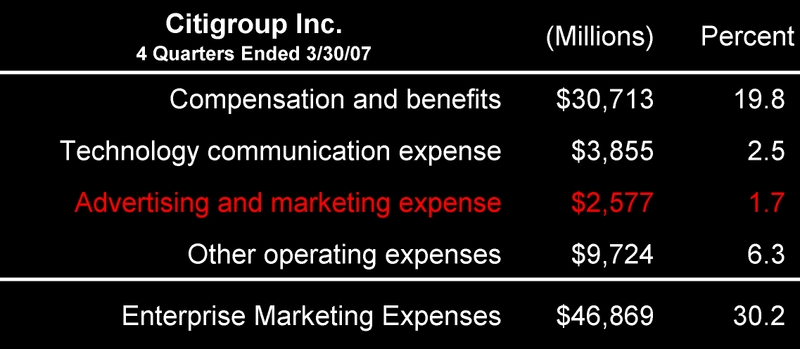

Everyone on the planet follows "The Top Line" and "The Bottom Line" performance of public companies. But do they ever look closely at "The Middle Line?" Rarely. What's the middle line? It is the resources and infrastructure Lehman Brothers brings to the table in cross-border and domestic deals. These resources and infrastructure are the enterprise marketing expenses that support Lehman’s sales revenue. In the last four quarters ending May 31, 2007 LEH's total revenues (including interest income) were $54,261 million. This table documents the $12,279 billion the company spent on enterprise marketing and its share of total revenues.

Each line item in this table is reported exactly as it appears in Lehman's 10-Q income statements from the EDGAR Online I*Metrix financial data service. Notice, that "Marketing" is not mentioned, except in the summary line I added at the bottom of this table. I suspect a lot of what appears in "Business Development" would fit in the traditional meaning of marketing – that is advertising expenses. But that's not the point. What matters is that every dollar was paid for people and activities that influenced how customers (and potential customers) and investors (as well as potential investors) perceived Lehman Brothers.

COST PER DOLLAR AND ENTERPRISE MARKET SHARES

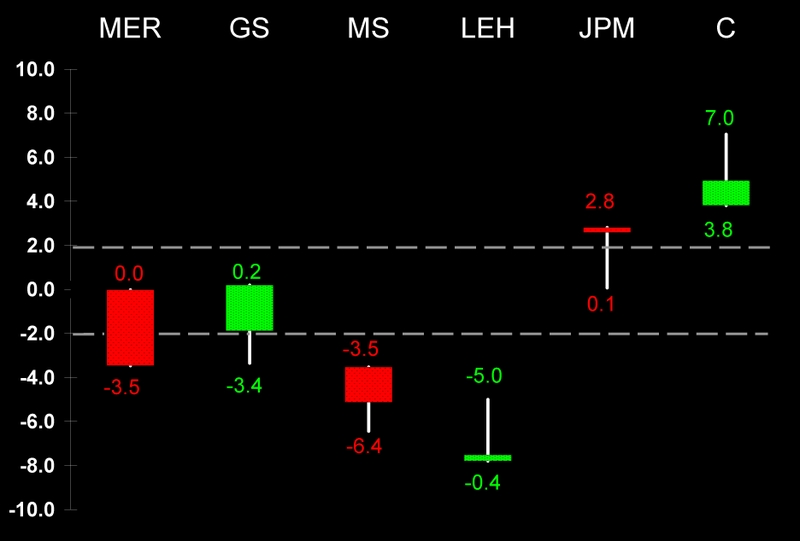

In the following chart I use the enterprise marketing expenses for Lehman and five major competitors to calculate their cost per dollar of revenue. The left-hand x-axis shows the ten most recent reporting periods beginning with February 28, 2005 and ending with May 31, 2007. The right-hand x-axis lists the six companies by their ticker symbols. Enterprise marketing costs per dollar of total revenue (including interest income) is on the Y-axis. [Click to enlarge charts]

In 58 of the 60 company-quarters Lehman had the lowest enterprise marketing expenses per dollar of revenue. And this chart shows it was not a result of scale economies.

Lehman Brothers had the lowest market share of all six firms over the ten quarters. Yet, it was the most efficient in generating revenues.

CANDLESTICK CHARTS OF TWO STRATEGIC GROUPS

To show the impact of mixing more heterogeneous competitors in a strategic group, I ran the analysis of risk-adjusted differentials (RAD) again with two changes in its membership:

- Lehman is added to the original group of five banks

- Both Citi and J.P. Morgan are removed from the group.

The risk-adjusted differential is standard-normal whole numbered index of a firm’s simultaneous performance in stock and product markets. For details on the theory and measurement see my 18 minute Adobe Connect presentation on "Y'All Buckle That Seatbelt." Or go back to the previous post in this series.

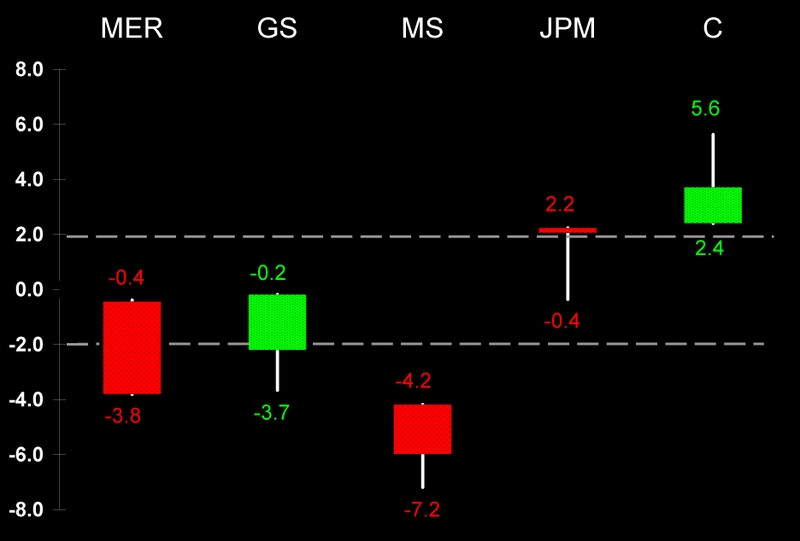

Candlestick charts are an efficient way to summarize the risk- adjusted differentials of all six companies over the ten quarters. In this chart three companies (GS, C and LEH) have green candles because they each have an ending RAD in March/May 2007 greater than a beginning RAD in December/March 2005.Three companies (MER, MS, and JPM) have red candles because they each have an ending value less than a beginning one. The size of a candle represents the spread between beginning and ending RADs and the wicks represent extreme departures from the beginning and ending numbers. The dotted lines are control limits of plus and minus two standard deviations from the expected value of RAD (zero).

In this group of six "investment banks" investors placed a significantly higher relative value on JPM and Citi then on the four other competitors. As it happens, JPM and Citi are the only ones with both significant consumer banking operations as well as investment banking operations. In fact, this is precisely what the viewer “VeryInterested” questioned in his or her comments on my posts. And it's a fair thing to question.

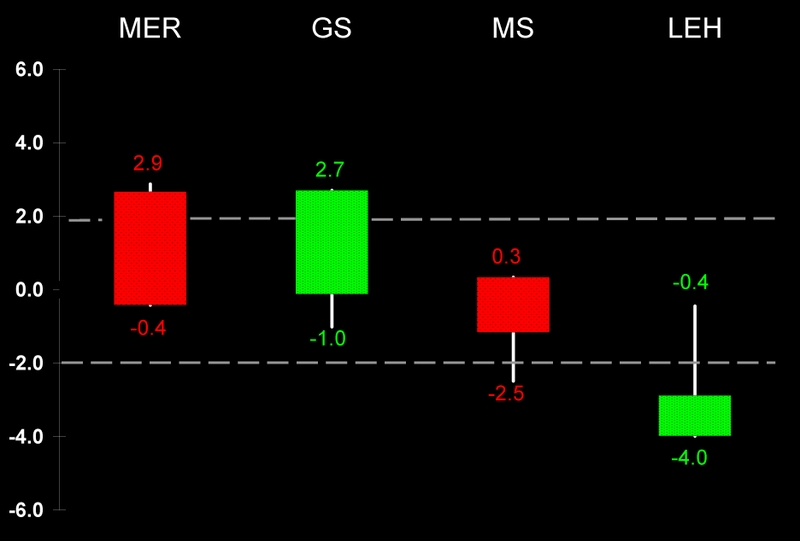

In this next chart I removed both JPM and Citi from the strategic group. For the most part, three of the four firms now are contained within the 95% confidence intervals of plus and minus two RADs.

But notice, the pattern is the same as in the previous chart: trends and rank orders are unchanged. Can Merrill Lynch management now be pleased with their performance? Not really. Should Lehman Brothers management be concerned? Yes. This final chart shows the time series for both.

The trend in Merrill's numbers remains unfavorable. And there's still that big drop in the last quarter. Lehman management, on the other hand, has more serious reasons for concern. Seven of its risk-adjusted differentials are less than -2.0. Just when it looked like investors had pulled LEH out of its slump, February, 2006 rolled around and things went downhill again.

VISIONS OF WHAT MIGHT BE

Strategic groups are inherently dynamic collections of companies that compete simultaneously for customers and capital. The companies that managers think are their competitors will change from year-to-year, if not from quarter-to-quarter.

You can't control the dynamic process behind strategic group formation. After all, a little over ten years ago Citibank would have been excluded from the group by law. At that time Citibank was prohibited from owning Smith Barney. For a short history of banking law see "The Long Demise of Glass-Steagall."

Today Citibank and Smith Barney are joined at the hip in a Boston test market. As the branch manager who runs the Citi Smith Barney side of the business said in Section 1, page 19 of its 2006 annual report: "It's exciting—and a little nerve-wracking—to pioneer new ways of growing our company and changing how we reach out to and serve clients."

The manager who runs the Citibank side of the business at the same branch agreed, saying: "If we're successful—and I've no doubt we will be—what we're doing here could help grow the business significantly. Imagine the possibilities when we put more and more of the company's resources and products at our clients' disposal."

Enterprise marketing analysis is not limited to what is. Its very essence is to visualize what might be, so you can make it happen ... if what you visualize makes sense. Does it make sense for Lehman Brothers, Morgan Stanley, Goldman Sachs, or Merrill Lynch to acquire significant consumer banking assets? What do you think?

In the future I'll compare the impact of changing strategic group membership other posts in this series. Stay tuned. Same time, same place.

Thank you for visiting.

~V

Great finds

- Casino Italiani Non Aams

- Nuovi Siti Casino

- Casinos Not On Gamstop

- Casinos Not On Gamstop

- Casino Sites Not On Gamstop

- Casino Online Non Aams

- Casino Online Non Aams

- Casino Sites Not On Gamstop

- Best Casinos Not On Gamstop

- Sites Not On Gamstop

- Non Gamstop Casinos UK

- Best Non Gamstop Casinos

- Non Gamstop Casinos UK

- Casino Sites Not On Gamstop

- UK Casino Sites Not On Gamstop

- UK Online Casinos Not On Gamstop

- Non Gamstop Casino

- UK Online Casinos Not On Gamstop

- Sites Not On Gamstop

- Non Gamstop Casinos

- Non Gamstop Casino Sites UK

- Non Gamstop Casinos UK

- Casinos Not On Gamstop

- Casino Non Aams Sicuri

- Casino Not On Gamstop

- Casino Online

- Meilleur Casino En Ligne Français

- Nouveau Casino Belge En Ligne

- I Migliori Casino Non Aams

- Casinos En Ligne France

- Casino En Ligne France

- Paris Sportif Ufc France

- топ крипто казино

- Miglior Sito Casino Online

- Casino En Ligne Qui Paye Vraiment

- Migliori Casino Online Italia

- Site Casino En Ligne

- Meilleurs Casino En Ligne

- Tortuga Casino

- Casino En Ligne

- Casinos En Ligne

- Casino En Ligne Argent Réel

- Casino En Ligne Retrait Immédiat

- Casino En Ligne

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}